Chargeback vs Refund: What's the Difference and Why It Matters

Understand the crucial differences between chargebacks and refunds for high-risk merchants. Learn cost comparisons, prevention strategies, and decision frameworks to protect your revenue.

"A refund is issued directly by the merchant to return a customer's money, while a chargeback is initiated by the customer's bank to forcibly reverse a charge."

Chargebacks typically cost merchants more through fees ($20-$50), harm chargeback ratios, and can threaten payment processing ability. High-risk merchants should prioritize refunds when appropriate to avoid the cascading costs of chargebacks.

The Core Distinction

Refunds occur when a merchant reverses a transaction, returning money directly to the customer. This happens through your payment system after a return or complaint. It's an agreement between merchant and customer. The merchant validates the issue, perhaps a returned product or service dissatisfaction, then processes the credit.

Chargebacks happen when customers bypass the merchant. They contact their credit card issuer to dispute a charge. The bank pulls funds from your merchant account. You don't initially have a choice. Chargebacks were designed as consumer protection against fraud, but now often include dissatisfaction scenarios.

Key Differences at a Glance

Who initiates: Refund is merchant-initiated (customer asks you, you issue credit). Chargeback is bank-initiated at customer request.

Parties involved: Refund involves 2 parties (customer and merchant). Chargeback involves 4+ parties (customer, merchant, issuing bank, acquiring bank, card network).

Cost to merchant: Refund means lost sale plus restocking; no extra fees. Chargeback means lost sale plus $20-$50 fee; counts against chargeback ratio.

Timeline: Refund is usually quick (days for customer to see credit). Chargeback is longer (weeks to months through formal dispute process).

Control: With refunds, you set policy and can offer alternatives (replacement, store credit). With chargebacks, the bank controls the process; you can only submit evidence.

Item return: With refunds, items are often returned to merchant. With chargebacks, customer often keeps item (especially in fraud cases).

Why High-Risk Merchants Must Understand This

In high-risk sectors, banks and card networks already view your business with more scrutiny. A high chargeback rate triggers monitoring programs that can damage your approval rates. These carry hefty fines or processing restrictions.

High-risk processors charge higher fees partly because chargebacks are more common. Every avoided chargeback saves more money. The margin for error is thinner. Choosing a refund when appropriate protects your whole operation, not just one transaction.

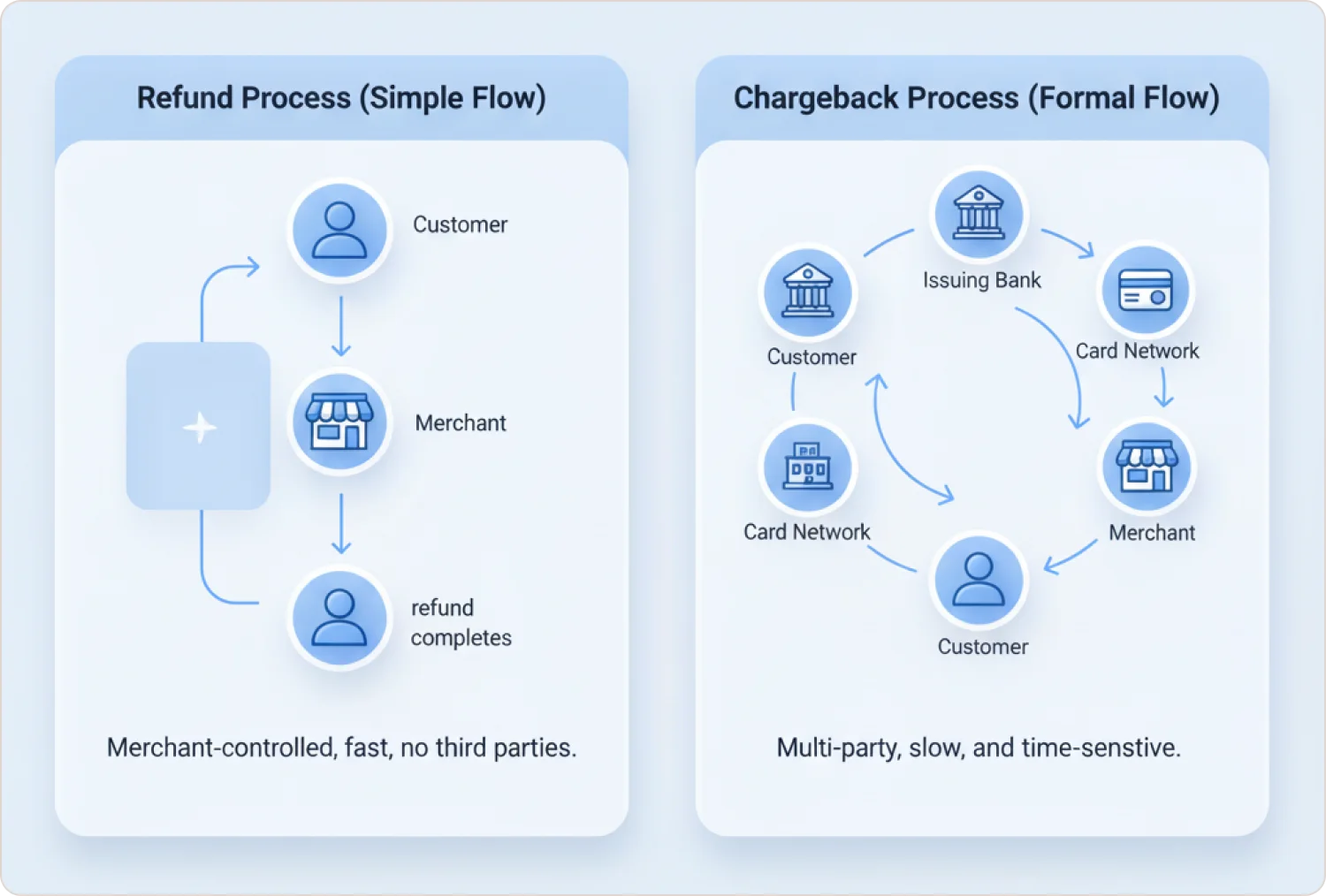

How Refund and Chargeback Processes Work

The Refund Process (Simple and Direct)

- Customer requests refund (contacts support or submits form)

- Merchant verifies request (checks if within policy, confirms product return if applicable)

- Merchant issues credit through payment gateway or POS

- Customer sees refund on bank statement within days

- Resolution complete (issue solved one-on-one)

No third-party intervention occurs. Partial refunds are possible (keeping restocking fees). The merchant maintains control throughout.

The Chargeback Process (Complex and Formal)

- Customer initiates dispute with issuing bank (claims reason like "item not received")

- Issuing bank provisionally credits customer and forwards chargeback through card network

- Merchant account debited; chargeback case opens with reason code notification

- Merchant decides: Accept the chargeback or contest via representment

- If contesting, merchant gathers evidence (proof of delivery, etc.) and submits to acquirer within deadlines

- Issuing bank reviews evidence; may escalate to arbitration if dispute continues

- Final outcome: Chargeback upheld (customer keeps money) or reversed (merchant wins, money returned minus potential fees)

Think of a chargeback like a formal legal case. The customer is the plaintiff. You're the defendant. Banks and Visa/Mastercard act as judges. A refund avoids this entire courtroom drama.

Why Speed Matters

The chargeback process is convoluted and time-bound. Merchants who don't respond within deadlines automatically lose. It's resource-intensive. Issuing a refund can often be completed in minutes.

Example: Imagine a customer unhappy with a late delivery. If they email you and you refund within 24 hours, that's resolved. If they instead call their bank, you might fight that $50 transaction for three months—and if you lose, you pay the amount plus a fee.

Refunds vs Chargebacks – Trade-Offs and Realities

Both Are Losses (But One Hurts More)

No merchant wants either outcome—both mean a lost sale. It's about damage control. Which option minimizes loss?

Cost Comparison

Refund: Lost revenue from the sale, maybe shipping costs. If the item returned in good condition, possibly resold (not total loss). No additional fees. A fair refund can sometimes increase future loyalty.

Chargeback: Lost revenue plus ~$20-$50 fee, plus staff time to handle it, plus potential increased processing fees if chargeback ratio climbs. Harm to reputation with processor. If you sell physical goods, you likely won't get the item back—customers often keep it. Chargebacks can be "item and money gone."

Time and Effort

Refund: Quick resolution, low effort (a few clicks). Processed within next payout cycle.

Chargeback: Potentially hours gathering documents, formulating responses, and waiting. Psychological strain—disputes are stressful and divert focus from running your business.

Customer Perception

Refund signals: "The merchant addressed my issue." This can salvage or even enhance loyalty.

Chargeback happens without merchant contact. You lose the chance to turn situations around. Relationship damage is greater.

"In the battle of refund vs chargeback, the refund is usually the lesser evil—it costs less, resolves faster, and doesn't endanger your ability to keep accepting payments."

Common Mistakes That Lead to Chargebacks (And How to Avoid Them)

Not all chargebacks come from devious fraudsters. Often, merchants' own slip-ups drive honest customers to file disputes. By fixing these mistakes, merchants save significant money.

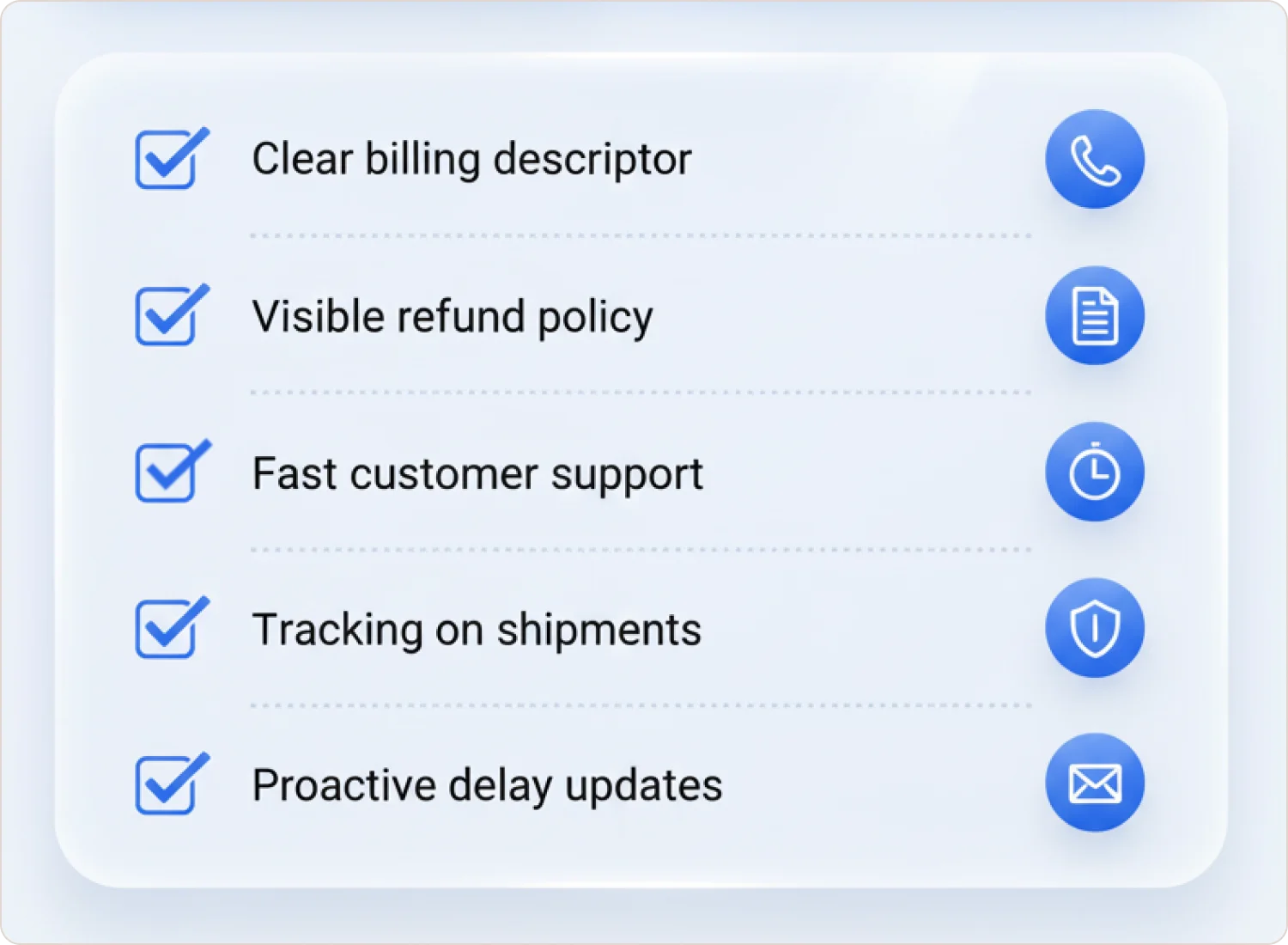

Mistake 1: Hiding or Complicating Refund Policies

If your refund process is a maze or nonexistent, customers go straight to the bank.

Fix: Publish a clear, accessible refund policy. For high-risk goods like supplements, make "30-day money-back guarantees" extremely visible. Include "If you're not happy, contact us—we'll make it right" on invoices.

Mistake 2: Unrecognizable Billing Descriptors

Customers often dispute charges they don't recognize on statements. If your business name is "ABC LLC" but you market as "GlamSkin Products," customers might not connect them.

Fix: Work with your payment processor to ensure billing descriptors are clear. Ideally include company name plus phone number (like "GLAMSKINPROD 800-123-4567").

Mistake 3: Slow or Poor Customer Service

When customers can't reach you easily or you respond slowly, they get frustrated and charge back out of impatience. Failed payment recovery strategies show that quick response times are critical.

Fix: Offer multiple support channels (email, phone, chat). Respond quickly with empathy. Even "we're looking into it" can slow customers from calling banks. Aim for 24-48 hour response times maximum.

Mistake 4: Not Using Tracking for Deliveries

Shipping products without tracking or signature confirmation on large orders lets customers claim non-receipt. It's hard to fight without proof.

Fix: Use tracking numbers. Require signatures for high-ticket items. Proactively send shipping updates.

Mistake 5: Lax Fraud Screening

Accepting fraudulent orders that slip through guarantees chargebacks. Merchants sometimes disable protections like 3-D Secure or AVS to reduce friction, then eat fraud losses.

Fix: Implement appropriate fraud prevention tools (AVS, CVV checks, fraud detection services). High-risk merchants face targeted fraud attempts, making this non-negotiable.

Mistake 6: Strict or Short Refund Windows

Offering only 7 days for returns can lead customers to chargeback after that period, since card rules allow 120 days to dispute.

Fix: Be flexible. Consider aligning refund policy closer to chargeback windows (60-90 days instead of 30, if feasible). This shows goodwill and undercuts chargeback timeframes.

Mistake 7: Not Communicating During Delays

Product delays or service outages without customer notification lead to impatience and disputes.

Fix: Proactively email or text about delays. Offer options (partial refund, bonus). Customers appreciate transparency.

Decision Guide – Should You Refund or Contest?

When disputes or complaints arise, merchants face choices: solve it (refund/replace) or potentially face a chargeback. Sometimes you must decide whether to contest a chargeback or accept it. Having a preset guide helps.

Handling Customer Disputes (Before They Become Chargebacks)

- Listen to the customer's issue. Gather facts. Is the request reasonable (item not received, defective) or suspicious?

- Check order details. Was AVS matched? Was the email suspicious? Prior dispute history from this customer?

- Is it within your refund policy? If yes, refund immediately—this is a no-brainer to avoid chargebacks.

- If you can't refund (or customer refuses resolution), try a last offer (replacement, store credit, partial refund). Document communications.

- If a chargeback is filed anyway, don't double refund. If you already refunded the customer and got a chargeback notice, gather proof of that refund to dispute it.

- Contest or accept decision. If it's fraud and you have proof (shipping tracking showing delivered), contest. If it's "buyer remorse" and you lack evidence, accepting might save time.

Learn more about identifying friendly fraud patterns.

Tips for Implementation

Teams (especially in high-risk with dedicated risk analysts) should train customer support on this flow. Support reps should know when to escalate cases to risk teams (signs of friendly fraud). Document decisions to identify repeat abusers. Teams that would rather hand escalations to an outside dispute specialist can start by comparing the top Chargebacks911 alternatives.

Platforms like Beast Insights help high-risk merchants unify payment data, monitor chargeback trends, and improve fraud detection across acquirers and gateways, making these decision frameworks easier to implement at scale.

Conclusion: Take Control of Your Payment Disputes

Understanding the difference between chargebacks and refunds isn't just payment processing trivia, it's the foundation of protecting your revenue and maintaining your ability to accept payments. For high-risk merchants, every chargeback avoided is a victory against mounting fees, damaged processor relationships, and potential account terminations.

Key Takeaways to Implement Today

- Prioritize prevention over cure. Clear billing descriptors, accessible refund policies, and responsive customer service prevent most disputes before they escalate.

- Choose refunds strategically. When facing borderline complaints, a $100 refund beats a $125+ chargeback loss every time.

- Build decision frameworks. Train your team to recognize when to refund immediately versus when to gather evidence for potential disputes.

- Monitor your metrics. Track your chargeback ratio religiously—if you're approaching 1%, take immediate action to implement stricter prevention measures. Understanding how to analyze approval rate drops can help you spot issues early.

The reality is simple: chargebacks are expensive, time-consuming, and damaging. Refunds, while not ideal, give you control. By implementing the strategies in this guide, you can significantly reduce chargebacks while maintaining customer satisfaction.

Frequently Asked Questions

Is a chargeback the same as a refund?

No. A refund is issued by the merchant directly to return a customer's money. A chargeback is initiated by the customer's bank, reversing the charge without the merchant's direct approval. Chargebacks involve banks and often include extra fees, unlike straightforward refunds.

Which is worse for a merchant: a chargeback or a refund?

Chargebacks are generally worse. They cost more (fees $20-$50+), harm your chargeback ratio, and can risk your ability to process cards. Refunds are voluntary and usually cost only the sale itself, making them far less damaging.

Why would a customer do a chargeback instead of requesting a refund?

Customers often choose chargebacks out of convenience or confusion. Studies show 84% find it easier to go to the bank than contact merchants. If they can't reach support quickly or don't recognize a charge, they might file a chargeback thinking it's the only option.

Can a merchant fight a chargeback?

Yes, through chargeback representment. Merchants can dispute chargebacks by submitting evidence to the bank that the sale was valid. However, fighting chargebacks is time-consuming and not guaranteed to succeed. Prevention is usually better. Merchants weighing an automated representment vendor for this can compare the main Justt alternatives.

Do refunds count against my chargeback ratio?

No. Refunds do not affect your chargeback ratio (they're not reported to card networks). Only actual chargebacks count. Issuing a refund can sometimes prevent a chargeback that would have counted against you. That's why proactive refunds protect your ratio.

What is refund abuse vs chargeback fraud?

Refund abuse is when customers exploit return policies (repeatedly returning used items). Chargeback fraud (friendly fraud) is when customers lie to banks to get charges reversed despite receiving products. Both are first-party fraud, but one uses merchant systems, the other uses bank systems.