Friendly Fraud in 2025: High-Risk Merchants' Guide to Prevention

Friendly fraud now represents 75% of chargebacks, up from 34% in 2023. Learn prevention strategies, new Visa VAMP rules, and how to fight back effectively.

What Is "Friendly Fraud" and Why Is It Rising?

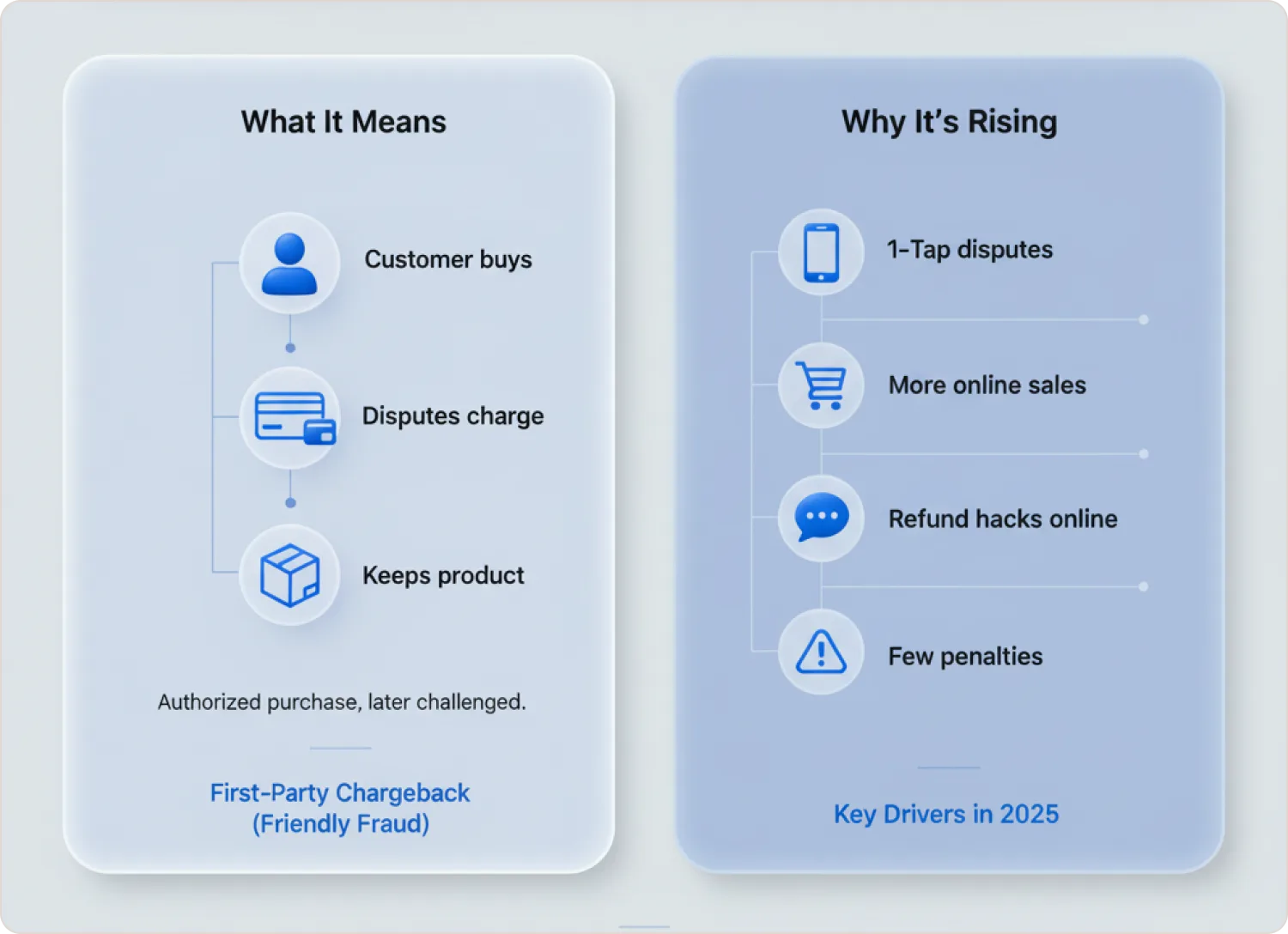

Friendly fraud occurs when customers dispute charges they actually authorized. Common examples include children making unauthorized game purchases, customers claiming refunds for delivered products, and subscribers disputing renewal charges.

Key Drivers

- Ease of filing disputes through banking apps

- E-commerce expansion post-2020

- Social media "refund hacks" normalizing the behavior

- Low perceived consequences for consumers

- 40% of Americans know someone who committed friendly fraud

Why High-Risk Merchants Are Hit Hardest

High-risk industries experience elevated chargeback rates across multiple verticals:

Subscription Services

Customers forget recurring charges or struggle with cancellation, defaulting to bank disputes instead.

Adult Entertainment

Privacy concerns drive cardholders to deny charges to avoid embarrassment.

Online Gaming & Digital Goods

Family fraud occurs when parents dispute children's purchases; digital products get consumed before chargebacks.

Travel & Ticketing

Non-refundable bookings get disputed when plans change.

CBD & Nutraceuticals

Subscription confusion combines with buyer's remorse.

Learn how failed payment recovery strategies can help reduce involuntary churn and recover revenue.

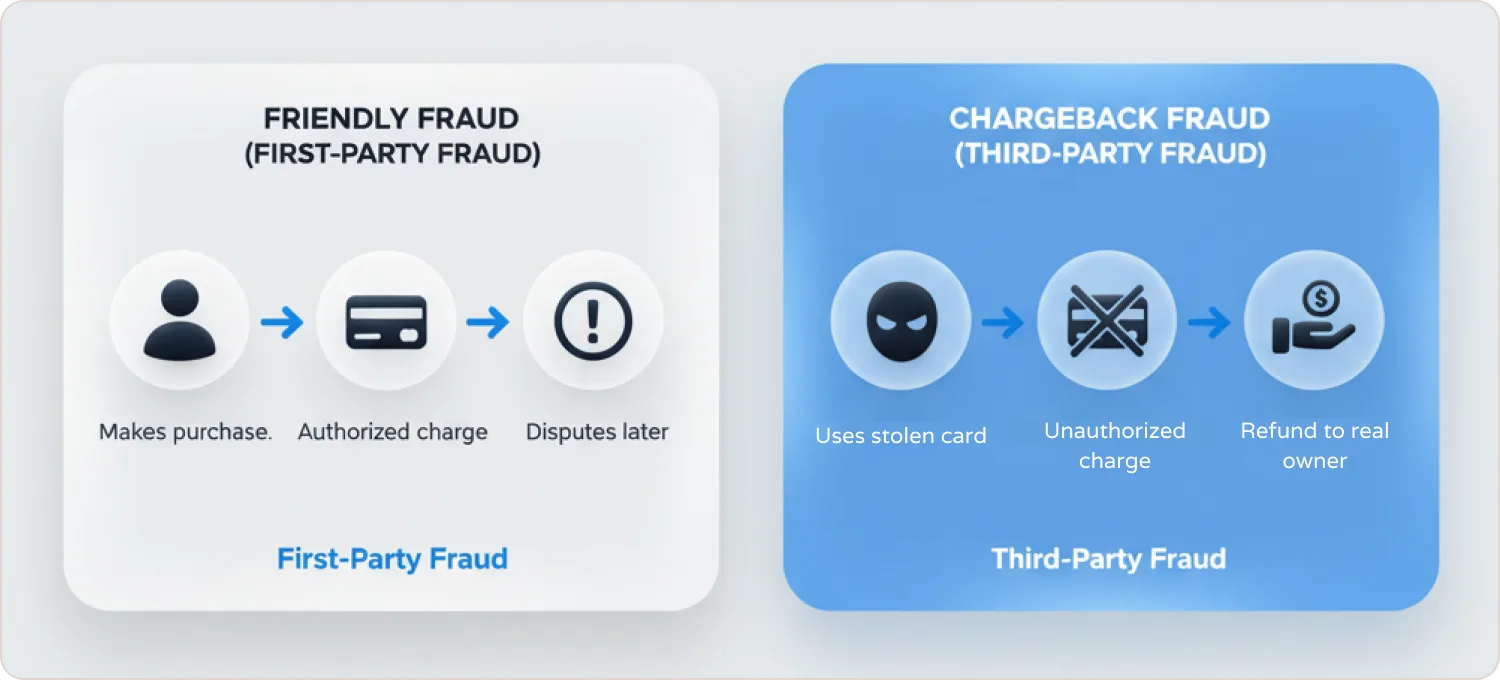

Friendly Fraud vs. Chargeback Fraud

Friendly Fraud (First-Party)

- Cardholder made the purchase

- Intent ranges from accidental to intentional

- Evidence includes delivery proofs and purchase agreements

True Fraud (Third-Party)

- Criminal uses stolen card

- Legitimate from cardholder's perspective

- Merchant had no authorization from real cardholder

Understanding the difference between chargebacks and refunds is crucial for building an effective dispute management strategy.

2025 Updates: New Rules & Tech

Visa VAMP

Visa replaced monitoring with the Visa Acquirer Monitoring Program in April 2025, enforcing stricter thresholds portfolio-wide.

Compelling Evidence 3.0

Mastercard Initiatives

Industry collaboration on data sharing between banks and merchants to identify patterns. According to Mastercard, money lost to chargebacks cost merchants an estimated $117.47 billion in 2023.

AI & Subscription Regulations

AI tools now analyze dispute patterns; clearer subscription disclosures and easy cancellation required by card networks. If you are shortlisting AI dispute automation, review the top Chargeflow alternatives alongside it.

How to Prevent Friendly Fraud

Prevention Checklist

- Clear Billing Descriptors - Include website or phone number on statements for recognition

- Immediate Order Confirmations - Send email/SMS summaries as timestamped evidence

- Delivery Tracking - Provide tracking info; follow up post-delivery

- Easy Refund Process - Offer simple returns to prevent chargebacks

- Responsive Customer Service - Reply within 24-48 hours to prevent frustration disputes

- Document Everything - Keep interaction records, delivery proofs, and IP addresses

- Leverage Fraud Tools - Use CVV checks, address verification, and 3-D Secure

- Blacklist Abusers - Block repeat offenders after multiple unwarranted chargebacks

- Analyze & Adapt - Treat chargebacks as feedback for operational improvement. Monitor your MID health to maintain strong approval rates while managing risk.

When Friendly Fraud Happens: Fighting Chargebacks

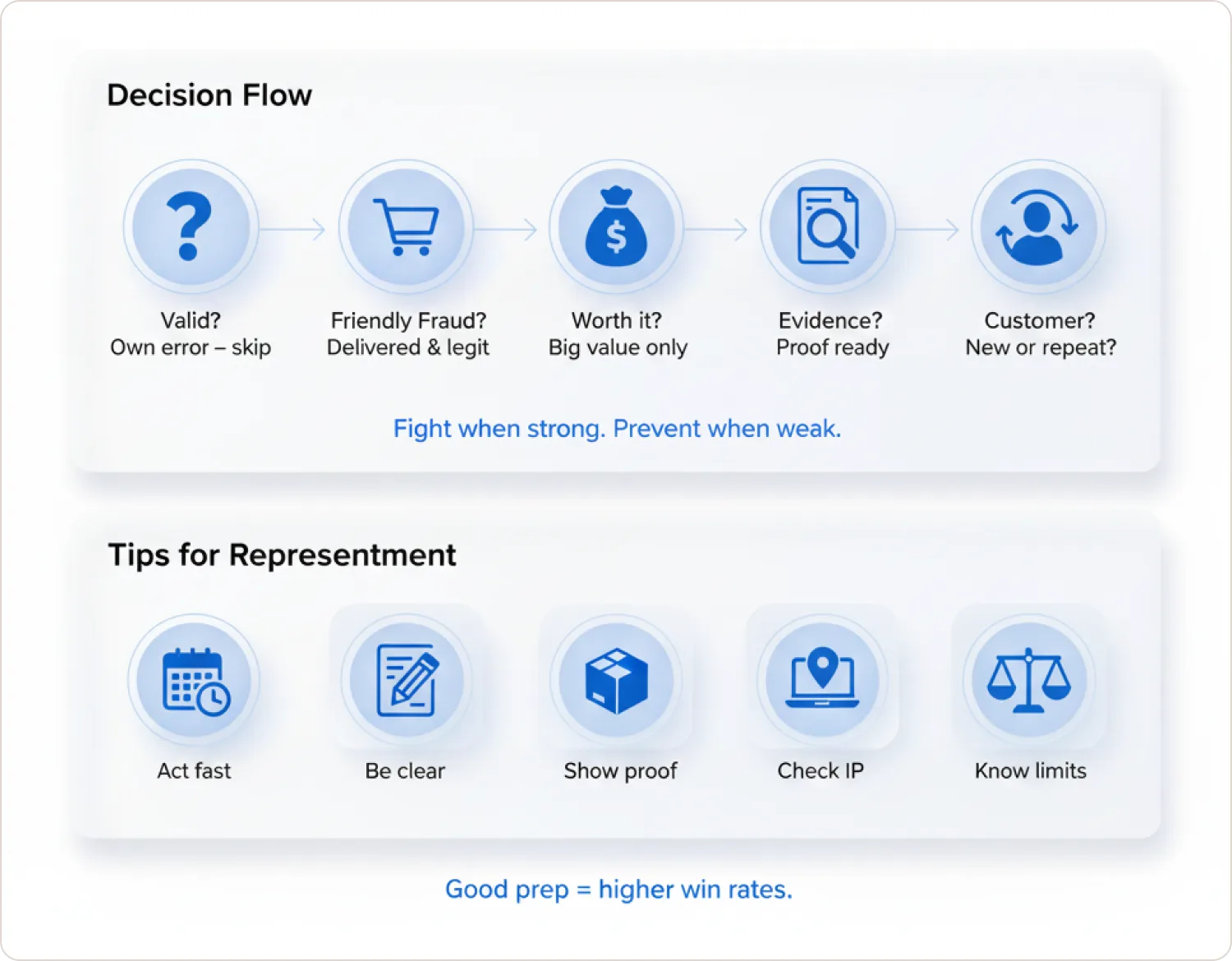

Decision Framework

- Is the chargeback valid? Accept and learn if merchant's fault

- Is it friendly fraud? Proceed if everything was legitimate

- Is it worth fighting? Consider amount vs. fees ($20 chargeback with $15 fees may not justify effort)

- Do you have evidence? Strong cases win ~43% of the time; weak cases around 20-30%

- What's the customer history? First dispute from good customer vs. repeat offender changes approach

Representment Tips

- Submit within 30-day deadline

- Include clear rebuttal letter with facts

- Provide delivery proof, order confirmations, login IP data

- Reference customer agreement screenshots

- Note prior transaction records (triggers Visa CE 3.0 auto-win)

Advanced Strategies: 4 Fraud Categories

Category 1: Authorized + Unintentional

Customer forgot or didn't recognize descriptor. Approach: Education and explanation.

Category 2: Authorized + Intentional

"Liar buyers" seeking free items. Approach: Fight with evidence and blacklist.

Category 3: Unauthorized + Unintentional

True fraud. Approach: Traditional prevention and 3-D Secure.

Category 4: Unauthorized + Intentional

Organized crime. Approach: Maximum vigilance and law enforcement collaboration.

Key Takeaways

- Prevention outperforms fighting: clear communication, responsive support, and easy refunds stop most disputes

- Document all interactions as chargeback evidence

- Categorize disputes by authorization status and intent to tailor responses

- Implement Visa CE 3.0 requirements for subscription businesses

- Collaborate through industry data-sharing initiatives

Conclusion

Friendly fraud is no longer a minor annoyance—it's a $132 billion problem that threatens high-risk merchants' ability to process payments. With 75% of chargebacks now classified as friendly fraud, prevention has become essential to survival.

The good news: merchants who implement comprehensive prevention strategies, leverage new tools like Compelling Evidence 3.0, and maintain strong documentation can significantly reduce their exposure and win more disputes when they occur.

The key is treating friendly fraud as an operational challenge to be managed, not an unavoidable cost of doing business. If you would rather outsource that management, weigh the strongest alternatives to Chargebacks911 before signing with any one vendor.

FAQ

What is a friendly fraud chargeback?

A friendly fraud chargeback occurs when customers dispute legitimate charges. They falsely claim purchases were unauthorized. The cardholder receives refund for valid transactions.

How is friendly fraud different from chargeback fraud by criminals?

Friendly fraud involves the legitimate cardholder (first-party). Chargeback fraud involves third-parties using stolen cards. With friendly fraud, the real cardholder authorized the transaction initially.

Why are high-risk businesses more prone to friendly fraud?

High-risk industries have characteristics that lead to disputes. Subscription services see forgotten charges. Adult content purchases get disputed for privacy. Gaming faces family purchases. These factors cause higher friendly fraud rates.

How can I prevent friendly fraud chargebacks?

Use clear billing descriptors. Send immediate receipts and confirmations. Provide easy refund options. Respond quickly to customer issues. Make it easy for customers to contact you first. Consider implementing pre-authorization charges to validate payments before fulfillment.

What should I do if I receive a friendly fraud chargeback?

Gather compelling evidence: delivery confirmations, usage logs, communications. Submit evidence through representment. Reach out to customer to understand their complaint. Analyze why it happened to prevent repeats.

Can chargeback alerts help stop friendly fraud?

Yes. Services like Verifi (Visa) or Ethoca (Mastercard) notify you before disputes formalize. This 24-72 hour window lets you resolve issues directly. You can refund to avoid formal chargebacks.

What is Visa Compelling Evidence 3.0 and how can it help?

Visa's CE 3.0 rule (effective 2023) helps fight friendly fraud. You can auto-win disputes by showing two prior successful transactions. Same customer, card, or device within 120 days proves legitimacy.

Are there penalties for customers who commit friendly fraud?

Yes. Banks track dispute patterns. Repeat offenders may have accounts closed. They get flagged in databases. Merchants blacklist them. Serial friendly fraudsters lose banking privileges and shopping access.