How a Pre-Authorization Charge Can Improve Customer Experience

Learn how pre-authorization charges help prevent revenue leaks, reduce chargebacks, and turn payment uncertainty into predictable cash flow for high-risk merchants.

One payment failure costs you the customer and their lifetime value.

Declined transactions cost U.S. businesses approximately $300 billion in lost revenue annually. Up to 42% of customers abandon purchases after experiencing a card decline.

For high-risk merchants, failed payments mean lost sales, damaged processor relationships, and wasted marketing spend. Pre-authorization charges offer a solution.

"The solution isn't processing more transactions. It's validating them before you ship."

Pre-authorization charges are temporary payment holds that verify fund availability before final billing. For high-risk merchants, they reduce payment failures, prevent chargebacks, and build customer trust through transparent billing practices.

What Is a Pre-Authorization Charge

Core Concept

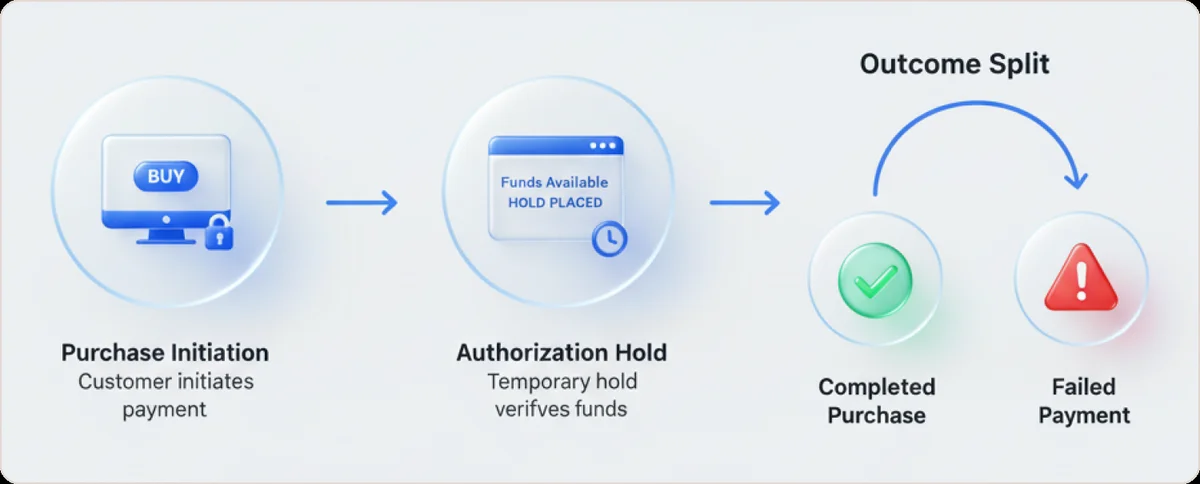

A pre-authorization charge (also called an authorization hold or preauthorization charge) is a temporary reservation on funds in a customer's account. No money leaves their account yet. Funds are earmarked but not captured.

Here's What Actually Happens

- Your customer clicks "Purchase"

- You request a hold for $100

- Their bank confirms: "Yes, these funds exist and this card is valid"

- $100 becomes unavailable to the customer but doesn't transfer to you yet

- You fulfill the order confidently

- You capture only the actual final amount ($85 if one item was unavailable)

- The $15 difference releases automatically

What You're Probably Doing Instead

- Customer clicks "Purchase"

- You charge the full amount immediately

- You ship the product

- Three days later, the charge fails

- You've lost the product, shipping costs, and payment processing fees

- Customer files a chargeback because "I never received it"

Why High-Risk Merchants Need Pre-Authorization

Pre-authorization validates genuine customers before fulfillment. The card isn't stolen and has available funds. Pre-authorization charges create a smooth customer experience by placing both parties on a more level playing field, reducing the risk of doubt and mistrust.

For industries facing elevated fraud and 2-15% chargeback ratios, pre-auth provides early validation that protects both revenue and processor relationships.

The reality for high-risk merchants:

- Card networks flag your MCC code for extra scrutiny

- Customers in your industry are more likely to dispute charges

- Processor relationships are fragile. Every chargeback counts

- Failed payments don't just lose revenue; they threaten your ability to process cards at all

How Pre-Authorization Actually Works (The Technical Reality)

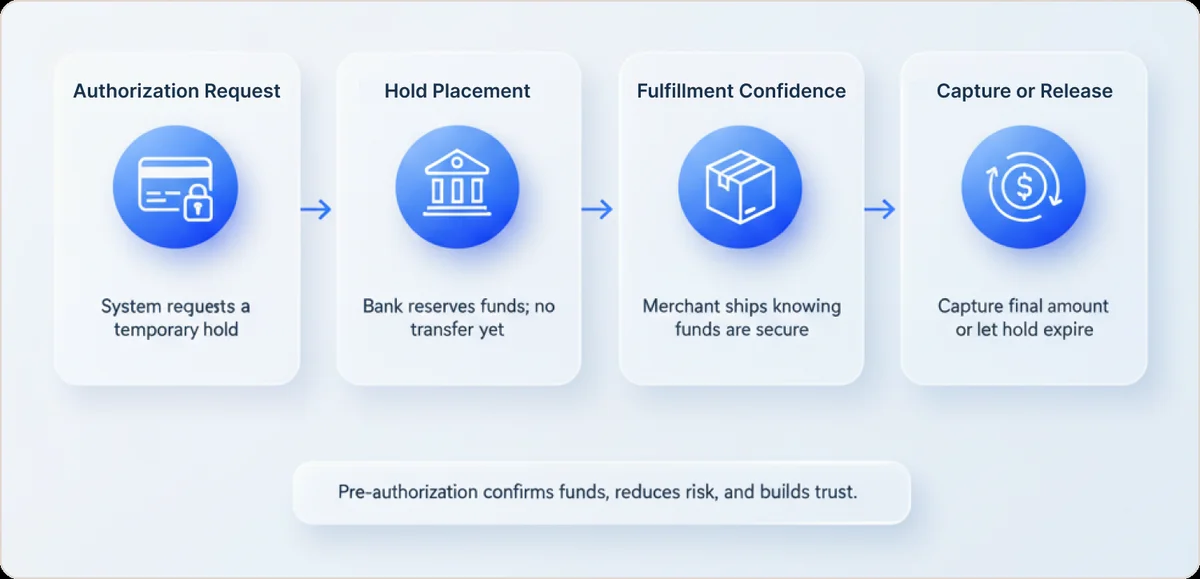

The Four-Step Process

Step 1: Authorization Request – Customer clicks "Purchase." Your system requests a hold for the estimated amount.

Step 2: Hold Placement – The issuing bank approves and places the hold, reducing the customer's available credit or funds by that amount. No money moves to you yet.

Step 3: Fulfillment Confidence – You receive approval confirmation. Now you can ship products knowing the funds are reserved, deliver services without payment risk, or request alternate payment immediately if declined (instead of discovering the problem after shipping).

Step 4: Capture or Release – If you fulfill: Capture the exact final amount within 5-7 days. If you can't fulfill: Let the hold expire. No refund processing needed. If the amount changes: Capture only what you actually charged; the rest releases automatically.

Benefits for Customer Experience

Preventing the 42% Abandonment Rate

When a customer's card declines after they've mentally "completed" the purchase, 42% never come back. They've moved on, found a competitor, or lost trust in your checkout process.

Pre-authorized payments validate funds at the moment of purchase intent. If there's a problem, the customer knows immediately while they're still engaged and motivated to complete the transaction.

Building Transparency That Converts to Trust

Your customers see pending charges in their account immediately. When explained properly, this creates confidence.

Effective messaging example: "We've placed a temporary $150 authorization (not a charge) on your card to verify your payment method. You'll only be billed $127.50 when your custom order ships on March 18th. If we can't fulfill your order, the hold releases automatically. No refund wait time."

Result: Customer understands exactly what's happening. Trust increases. Support tickets decrease.

Reducing Chargebacks Before They Happen

What is a pre-authorization charge doing in the background that you don't see?

- Confirming the card isn't stolen

- Verifying sufficient funds exist

- Creating a paper trail that the customer authorized the transaction

- Giving customers time to contact you before the charge processes

Pre-authorization is a critical defense against friendly fraud, which now accounts for 75% of all chargebacks. By validating transactions upfront, you create documentation that proves customer intent and reduces dispute vulnerability.

Eliminating Double-Processing Nightmares

The old way (authorization charge + refund): Charge $100, customer cancels, refund $100. You pay processing fees on both the charge AND the refund.

The pre-auth way: Authorize $100, customer cancels, hold releases. You pay zero fees.

Savings: $2.50-$3.50 per canceled transaction. For merchants with 200+ monthly cancellations, that's $6,000-$8,400 in annual savings on processing fees alone.

Understanding the difference between chargebacks and refunds becomes critical when implementing pre-authorization strategies—you're essentially preventing the need for both.

Customer Peace of Mind

"I ordered something, they couldn't deliver it, and I didn't have to wait 5-7 business days for a refund" is worth its weight in gold for customer lifetime value.

Practical Implementation Considerations

Setting Hold Amounts

Authorize slightly above expected totals but avoid over-authorization. High holds tie up customer funds unnecessarily. Authorize what you reasonably expect plus 10-15% cushion.

Communication Is Critical

Most customer frustration stems from not understanding holds. Provide clear checkout messaging: "We'll place a temporary $[X] hold (not a charge) on your card. You'll only be billed when your order ships. Holds release within 5-7 days if not captured."

Operational Monitoring

Ensure captures happen before holds expire. Set dashboard alerts for authorizations nearing expiration. Automate capture upon fulfillment triggers. Miss this window and you'll need to re-authorize—creating friction.

When Not to Use Pre-Auth

Skip pre-auth for instant digital delivery with fixed prices or low-cost items with immediate fulfillment. Use strategically where it solves problems: uncertain totals, fulfillment delays, or card verification needs.

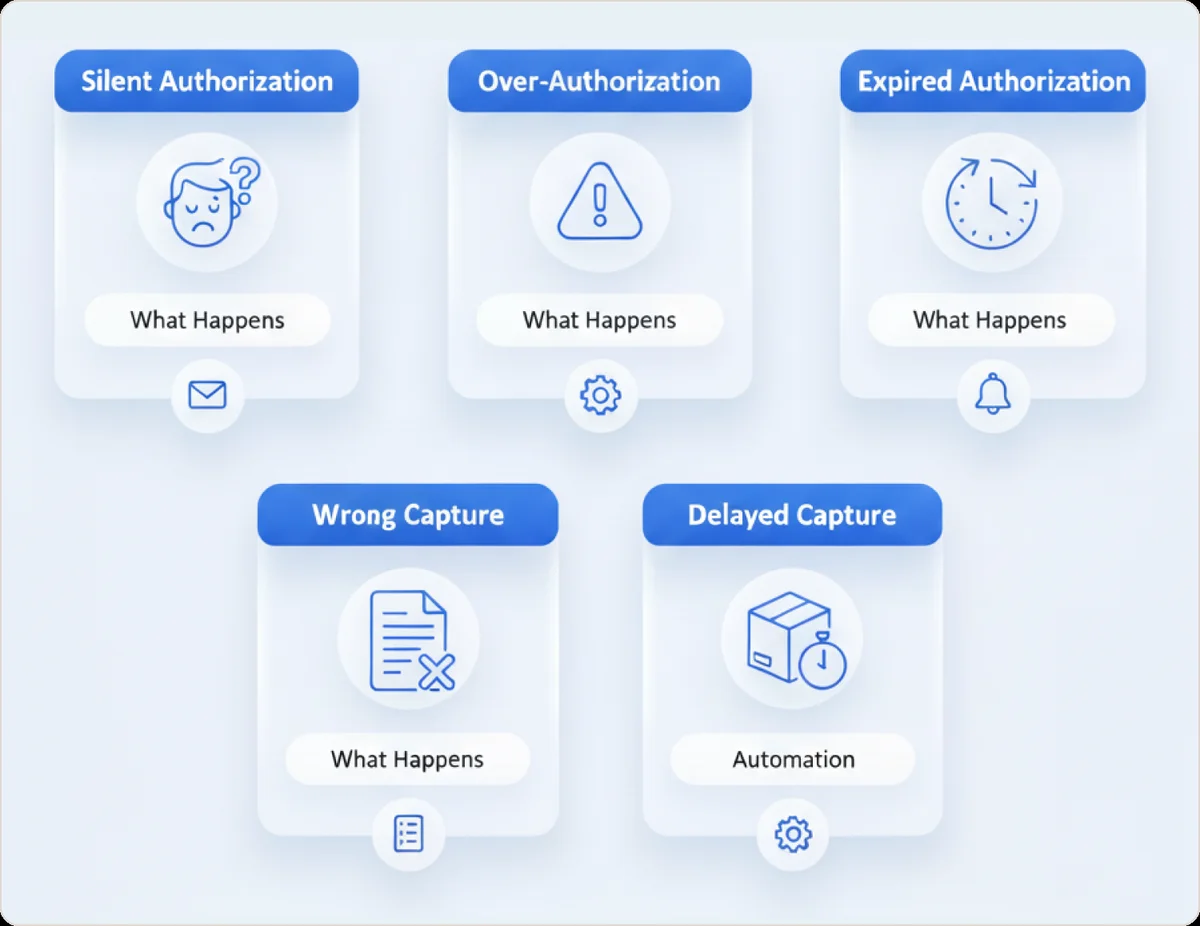

Common Mistakes That Cost You Money

Mistake #1: Silent Authorization (Not Informing Customers)

What happens: Customer sees pending charge, doesn't understand it, calls bank, files dispute.

The fix: Include checkout and email explanations every time.

Mistake #2: Authorization Paranoia (Over-Authorization)

What happens: You authorize $500 for orders averaging $100, customers see the huge pending charge and freak out.

The fix: Authorize expected amount + 10-15% buffer maximum.

Mistake #3: Authorization Amnesia (Letting Holds Expire)

What happens: Authorization expires before you capture, requiring re-authorization and creating friction.

The fix: Automate capture triggers based on fulfillment events; set up expiration alerts.

Mistake #4: Authorization Generosity (Forgetting to Capture)

What happens: You ship products but never capture payment. Basically giving away inventory.

The fix: Automate capture immediately upon shipment confirmation.

Mistake #5: Authorization Ignorance (Not Tracking Performance)

What happens: You implement pre-auth but have no visibility into which authorizations fail, why they fail, or which processors perform best.

The fix: Implement unified payment intelligence to see the full picture.

Smart Routing: The Authorization Multiplier Effect

You can implement preauthorization charges perfectly and still lose 15-20% of authorization requests unnecessarily.

Why Authorization Requests Fail (Even with Valid Cards)

- Processor A has a poor relationship with certain issuing banks

- Your MCC code triggers elevated scrutiny at specific acquirers

- Time of day affects approval rates (bank system maintenance, batch processing)

- Geographic routing paths have higher decline rates

Understanding why approval rates drop and how to diagnose the root cause is essential for optimizing your authorization strategy.

Smart Routing Solves This By

- Attempting authorization through Processor A

- Detecting the decline in real-time

- Automatically retrying through Processor B (which has better relationships with that card's issuer)

- Capturing the authorization success and learning from the pattern

Smart routing works hand-in-hand with maintaining healthy MID relationships, as processor performance directly impacts authorization approval rates.

Implementation Checklist

- Enable auth-only mode in your payment gateway settings

- Document hold policy internally (amounts, duration, capture timing)

- Create customer communication templates for checkout and emails

- Train support team on explaining holds positively

- Set up monitoring with alerts for expiring authorizations

- Automate capture triggers linked to fulfillment events

- Establish contingency procedures for declined or expired authorizations

Compliance Note (What You Must Disclose)

Visa and Mastercard require disclosure of authorization hold amounts at checkout. Failure to disclose can result in processor penalties.

According to Visa's merchant guidelines and Mastercard's acceptance rules, merchants must provide clear authorization disclosure to comply with card network requirements.

Industry-Specific Requirements

- Gaming/gambling: Explicit consent for hold amounts required

- Telecom: Specific disclosure formatting mandated

- Subscriptions: Clear communication of recurring authorization charges

Required Elements in Your Disclosure

- Hold amount

- Duration (typically 5-7 days)

- Difference between hold and final charge

- When final charge processes

Conclusion: Turn Payment Uncertainty Into Predictable Revenue

Pre-authorization charges transform payment uncertainty into predictable revenue. When implemented with clear communication, they prevent failures, build trust, and protect against fraud.

But pre-authorization alone is only part of the solution. Without payment intelligence showing you which authorizations fail, when to retry them, and how to route them optimally, you're still leaving money on the table.

Frequently Asked Questions

What is a pre-authorization charge?

A temporary hold on a customer's card that reserves funds without charging them until final capture.

How do pre-auths improve customer experience?

They prevent payment surprises by not charging until delivery, eliminating double-charge-refund scenarios and building transparency.

Do pre-authorizations reduce chargebacks?

Yes. They confirm funds and customer intent upfront, screening out fraud and creating documentation that defends against disputes.

How long do pre-authorization holds last?

Typically 5-7 days. Some industries get longer with proper merchant category codes. Capture before expiry or the hold releases.

Are customers charged fees for pre-authorization?

No. Pre-auth is a hold, not a charge. No additional fees apply to customers.

What businesses should use pre-auth holds?

Those with uncertain final totals, fulfillment delays, or high no-show risk—hotels, car rentals, high-risk e-commerce, subscriptions.