VAMP Thresholds Explained: Visa Acquirer Monitoring Program

The current VAMP thresholds after the 1 April 2026 tightening: the Excessive Merchant line is now 1.50% (150 bps) across the US, Canada, EU, APAC, and LATAM, with CEMEA the lone holdout at 2.20%. Includes the ratio calculation, the RDR carve-out, remediation timeline, and how to stay under the line.

Your VAMP playbook is out of date if it still treats 2.20% as the merchant line. On 1 April 2026, Visa dropped the Excessive Merchant threshold to 1.50%. That change is now in force across most of the world. This post is the thresholds-and-calculation deep dive. For the plain-English overview, see what the Visa Acquirer Monitoring Program is.

What are the current thresholds for the Visa Acquirer Monitoring Program (VAMP)? As of 2026, a merchant is Excessive at a VAMP ratio of 1.50% (150 basis points) in the US, Canada, the EU, APAC, and LATAM. CEMEA is the exception and stays at 2.20%. At the acquirer level, the portfolio line holds at 0.50% Above Standard and 0.70% Excessive.

What VAMP is and how it replaced VDMP and VFMP

VAMP is Visa's consolidated program for monitoring card-not-present fraud and disputes on a single combined ratio. Effective 1 April 2025, it folded five prior fraud-and-dispute programs into one acquirer program. It also streamlined 38 separate remediation processes into a single process. Visa now scores fraud and disputes together, not as two independent metrics.

Before VAMP, Visa ran two separate merchant programs. The Visa Dispute Monitoring Program (VDMP) tracked chargeback ratios. The Visa Fraud Monitoring Program (VFMP) tracked fraudulent transactions. Visa retired both and consolidated them into VAMP in 2025. So any target still tuned to a standalone VDMP dispute rate or a separate VFMP fraud ratio is chasing a threshold that no longer exists.

Current VAMP thresholds (2026): merchant and acquirer lines now in effect

Here are the exact Visa Acquirer Monitoring Program (VAMP) thresholds in force in 2026. The merchant Excessive line is 1.50% (150 bps) in the US, Canada, the EU, APAC, and LATAM. It is 2.20% in CEMEA. Acquirer portfolios are Above Standard at 0.50% and Excessive at 0.70%. A merchant only enters assessment above a floor of 1,500 combined fraud-and-dispute events per month.

| Level / metric | Threshold now | Region & notes |

|---|---|---|

| Merchant, Excessive (VAMP ratio) | 1.50% (150 bps) | US, Canada, EU, APAC, LATAM. 1.50% since 1 Apr 2026 for the first four (replaced 2.20%); LATAM was already at 1.50%. |

| Merchant, Excessive (CEMEA) | 2.20% (220 bps) | CEMEA only, the single region not reduced on 1 April 2026. |

| Merchant, minimum count floor | ≥ 1,500 events / month | Combined fraud + dispute count; below this, a merchant is excluded from VAMP. |

| Acquirer, Above Standard | 0.50% (50 bps) | Portfolio VAMP ratio. Unchanged in 2026; holds from the April 2025 launch. |

| Acquirer, Excessive | 0.70% (70 bps) | Portfolio VAMP ratio. Unchanged in 2026. |

| Enumeration ratio | 20% (2,000 bps) | Enumerated auth transactions / total, with a 300,000-transaction floor. |

Merchant Excessive line per Visa's fact sheet and vendor confirmations; 1.50% is the current value since 1 April 2026, 2.20% now applies only in CEMEA. Acquirer tiers unchanged from the 2025 launch.

One nuance trips people up. The 2.20% figure is not wrong. It is simply historical for most of the world. It applied in the US, Canada, EU, and APAC from the 1 October 2025 enforcement start until 31 March 2026. LATAM was always at 1.50%, and 2.20% survives today only in CEMEA. Everywhere else, the current excessive merchant threshold is 1.50%, and remediation triggers now fire there. Tracking this per merchant ID (MID) against Visa's line is exactly what card scheme compliance monitoring is for.

Above-standard vs excessive tiers, and the fees at each

How do the above-standard and excessive tiers differ? At the acquirer level, a portfolio is Above Standard at a VAMP ratio of 0.50% and Excessive at 0.70%. Both tiers carry per-transaction fees that escalate at the higher line. Merchants are identified against their own 1.50% Excessive line. The pressure flows through the acquirer that owns the MID.

| Tier | Ratio | Per-transaction fee (vendor-reported) | What it means |

|---|---|---|---|

| Acquirer, Above Standard | 0.50% (50 bps) | $4 per TC40 / TC15 | Acquirer must investigate and remediate across the portfolio. |

| Acquirer, Excessive | 0.70% (70 bps) | $8 per TC40 / TC15 | Fees double; Visa scrutinizes individual merchants in the portfolio. |

| Merchant, Excessive | 1.50% (150 bps) | $8 per TC40 / TC15 | Acquirer may restrict, reserve, or offboard the merchant. |

Ratio bands per Visa's fact sheet, which publishes only ratio thresholds, no dollar fees. The $4 / $8 per-transaction amounts come from vendor sources (Chargebacks911, NMI, Chargeback Gurus), and acquirers set their own fees in practice.

On the fees: Visa's public fact sheet publishes only ratio-based thresholds and no per-transaction dollar amounts. Vendor sources report a $4 fine on every fraud report (TC40) and dispute (TC15) at the acquirer Above Standard tier. That doubles to $8 at Excessive, and excessive merchants are also assessed $8 per transaction. These fees have been in effect since enforcement began on 1 October 2025. Acquirers set their own schedules, so treat the $4/$8 figures as the reference ratio, not a fixed invoice.

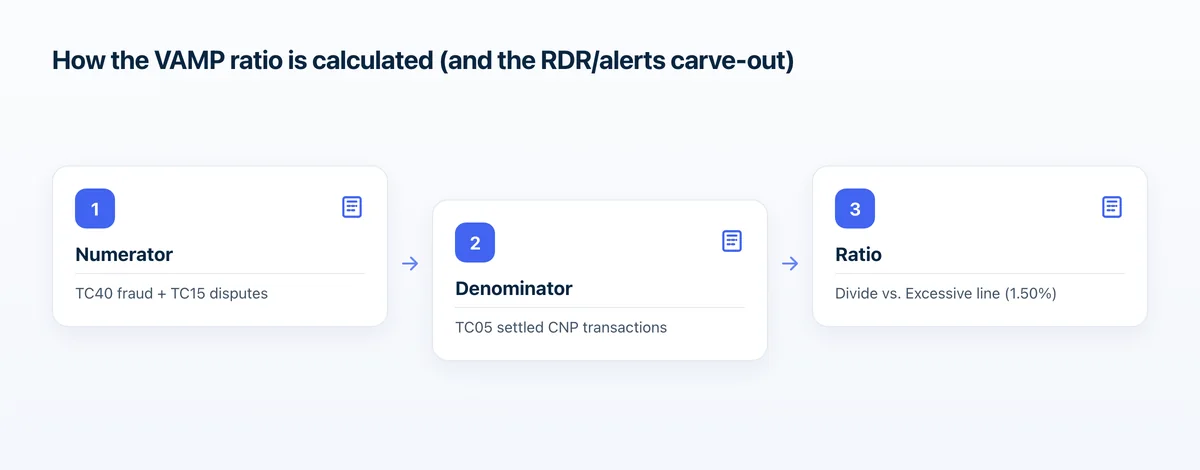

How the VAMP ratio is calculated (and the RDR/alerts carve-out)

How is the VAMP ratio calculated? It is a single count-based metric. It divides the count of Fraud (TC40) plus Disputes (TC15) by the count of Settled Transactions (TC05), on card-not-present VisaNet volume, measured monthly. Because it counts events rather than dollars, a low-value disputed transaction weighs exactly the same as a high-value one.

Here is the carve-out most merchant content gets wrong. Visa's ratio excludes disputes resolved through pre-dispute solutions. It also excludes TC40 fraud qualified for Compelling Evidence 3.0. But Rapid Dispute Resolution (RDR) and the Cardholder Dispute Resolution Network (CDRN) only cancel the TC15 dispute. The TC40 fraud report for that same transaction still counts. Only Compelling Evidence 3.0, submitted through Order Insight and accepted by the issuer, removes the TC40 signal.

A worked example: is a merchant over the line?

Let's run the math on a clearly hypothetical merchant. Say a merchant runs 200,000 card-not-present transactions a month with 2,600 combined TC40 fraud reports and TC15 disputes. These volumes are an illustrative example, not a real customer. Dividing 2,600 by 200,000 gives a VAMP ratio of 1.30%. That is under the current 1.50% line, but not by much.

- Numerator: 2,600 combined TC40 fraud + TC15 dispute events for the month.

- Denominator: 200,000 settled card-not-present transactions.

- Ratio: 2,600 / 200,000 = 0.013 = 1.30% (130 bps), and the count clears the 1,500-event floor, so this merchant is in scope for assessment.

- Verdict: below the current 1.50% Excessive line, but a single bad month adding ~400 more events would push it to 1.50% and over.

Consider two things about this example. First, at the old 2.20% line this merchant looked comfortable. At 1.50%, it is one campaign away from Excessive. Second, say even 200 of those 2,600 events are RDR-eligible disputes resolved in-month. Deflecting them drops the ratio to 1.20% (2,400 / 200,000), remembering that any linked TC40 still counts.

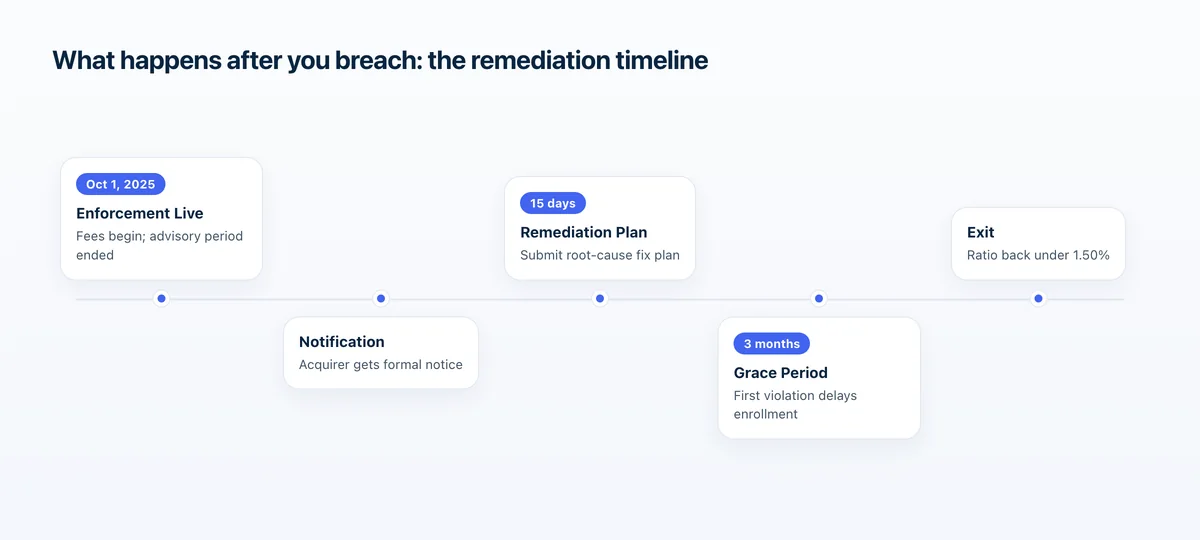

What happens after you breach: the remediation timeline

What happens after you breach a VAMP threshold? Merchants are not directly subject to VAMP. Enforcement flows through the acquirer that owns the MID. Visa notifies the identified acquirer, which must respond and submit a remediation plan. First-time violations within a rolling 12-month period get a three-month grace period. The mechanics below come from vendor descriptions of the Visa process.

For merchants, the sharpest consequence is upstream. Acquirers face per-transaction fines across their whole portfolio once Above Standard or Excessive. So they have a strong incentive to restrict or offboard merchants whose individual ratios threaten portfolio compliance. That pressure can escalate to mandatory reserves, account termination, and placement on the MATCH list, a shared blacklist of terminated merchants. Keeping MID health and approval rates in view matters as much as the raw ratio.

How to lower your VAMP ratio: prevention alerts + representment

How do you get your VAMP ratio down? Because the ratio is count-based, the levers are simple to state. Remove qualifying disputes from the numerator before they post, and win back the ones that do. Visa excludes disputes resolved through pre-dispute solutions and TC40 fraud qualified for Compelling Evidence 3.0. So prevention alerts and evidence-backed representment move the number directly.

- Deploy RDR to auto-resolve eligible disputes before they become TC15 records, removing them from the dispute count (the linked TC40 still counts).

- Layer CDRN and Ethoca prevention alerts to catch disputes the issuer flags before they hit the network.

- Pursue Compelling Evidence 3.0 through Order Insight on qualifying fraud so the TC40 report itself can be excluded.

- Represent disputes you can win with order, delivery, and login evidence to recover revenue and demonstrate remediation.

- Break your ratio down by gateway/MID, acquirer, issuing bank, BIN, card brand, and billing cycle to find where disputes concentrate.

- Watch enumeration traffic separately so a BIN attack does not trip the 20% / 300,000 enumeration track.

- Model every MID against the current 1.50% line, not the retired 2.20%, the margin is thinner than it was in 2025.

This is the layer Beast operates in. As a Visa Verifi reseller, Beast provides RDR, CDRN, and Ethoca prevention alerts plus chargeback representment. Only effective alerts, those that provably prevented a chargeback, are billable, and effectiveness is shown in-report rather than promised. Beast is the monitoring, measurement, and alert-deflection layer that helps keep a dispute-plus-fraud ratio under the VAMP line. It does not guarantee compliance.

VAMP vs Mastercard monitoring programs at a glance

How does VAMP compare to Mastercard's programs? Visa's VAMP merges fraud and non-fraud disputes into one combined count-based ratio. Mastercard keeps fraud and chargebacks as separate programs and gates on both a ratio and an absolute count. Its Excessive Chargeback Merchant tier triggers at a 1.5% ratio and 100 chargebacks per month, sustained across two months.

| Dimension | Visa VAMP | Mastercard ECM | Mastercard HECM |

|---|---|---|---|

| Scope | Fraud (TC40) + disputes (TC15) combined, CNP | First-presentment chargebacks, any reason code | Chargebacks, any reason code |

| Trigger | 1.50% ratio (2.20% CEMEA) | 100–299 chargebacks AND 1.5%–2.99% ratio | 300+ chargebacks AND 3%+ ratio |

| Metric type | One combined ratio | Ratio AND count (both required) | Ratio AND count (both required) |

| Sustained over | Monthly assessment | Two months | Two months |

| Exit | Ratio back below the line | Three consecutive compliant months | Three consecutive compliant months |

Visa figures per Visa's fact sheet and vendor confirmations; Mastercard ECM/HECM figures per vendor sources. Key difference: Mastercard needs BOTH a ratio and a count to breach and keeps fraud (EFM) separate; VAMP uses a single combined ratio.

The structural difference matters operationally. VAMP's single combined ratio means one fraudulent transaction can hit you twice, once as a TC40 and once as a TC15. Mastercard's Excessive Chargeback Merchant (ECM) program instead requires a MID to exceed both the chargeback count and the ratio to be noncompliant. It keeps its Excessive Fraud Merchant program on a separate fraud-only track with its own four-part test.

What is the current VAMP threshold for merchants?

The merchant Excessive VAMP threshold is 1.50% (150 basis points) as of 2026, in effect in the US, Canada, the EU, APAC, and LATAM. CEMEA is the only region still at 2.20%. A merchant also needs at least 1,500 combined fraud-and-dispute events in the month to be assessed at all.

When did the VAMP threshold drop to 1.5%?

The Excessive Merchant VAMP ratio dropped from 2.20% to 1.50% on 1 April 2026, and it is now in force across the US, Canada, the EU, APAC, and LATAM. The earlier 2.20% figure applied from the October 2025 enforcement start until 31 March 2026, and it survives today only in CEMEA.

How is the VAMP ratio calculated?

The VAMP ratio is the count of Fraud (TC40) plus Disputes (TC15) divided by the count of Settled Transactions (TC05), on card-not-present VisaNet volume, measured monthly. It is count-based, so every disputed transaction weighs the same regardless of dollar value, and the numerator and denominator come from the same month.

Does RDR reduce my VAMP ratio?

Partly. Rapid Dispute Resolution removes the TC15 dispute from the numerator, but the TC40 fraud report for that same transaction still counts. Only Compelling Evidence 3.0, submitted through Order Insight and accepted by the issuer, removes the TC40 signal. For an RDR exclusion to apply, both the dispute and its resolution must fall in the same month.

What are the VAMP acquirer thresholds?

The acquirer portfolio thresholds are 0.50% (50 bps) for Above Standard and 0.70% (70 bps) for Excessive. These did not change in 2026; they hold from the program's April 2025 launch. Vendor sources report $4 per TC40/TC15 transaction at Above Standard and $8 at Excessive, though acquirers set their own fee schedules.

How is VAMP different from Mastercard's chargeback program?

VAMP combines fraud (TC40) and disputes (TC15) into one count-based ratio. Mastercard runs separate programs and requires both a ratio and an absolute count to breach: its Excessive Chargeback Merchant tier triggers at a 1.5% ratio and 100 chargebacks per month, sustained across two months, while fraud sits on a separate Excessive Fraud Merchant track.