The $347K Revenue Recovery Plan: Smart Payment Retry Strategies for Subscription Businesses

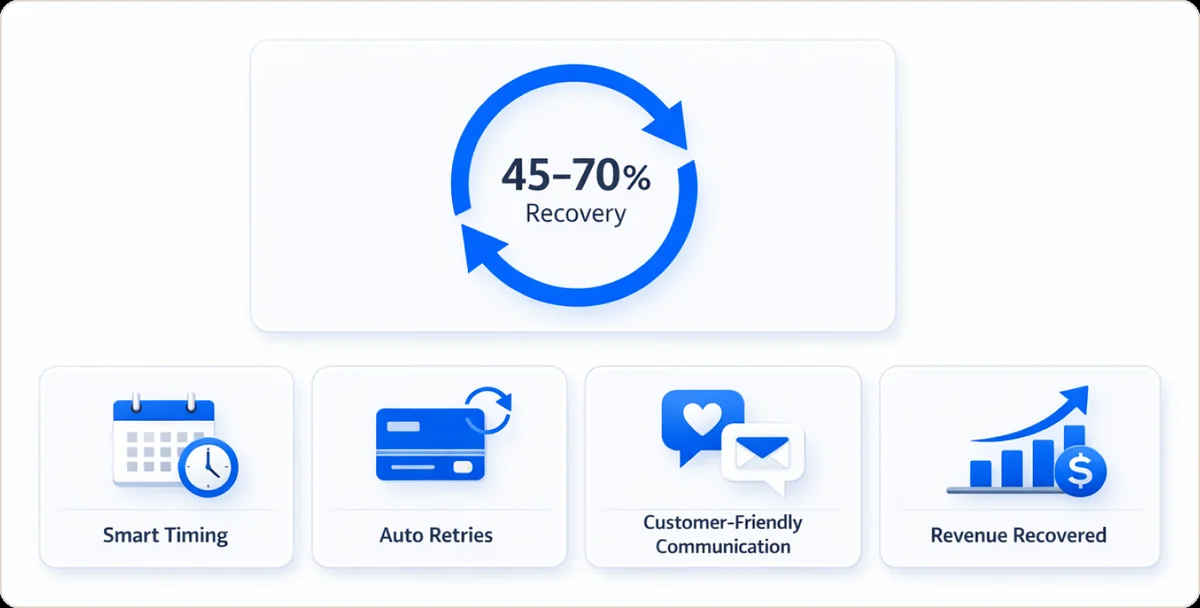

Payment retry strategies automatically recover 45-70% of failed subscription payments through intelligent timing, soft decline analysis, and proactive customer communication—protecting thousands in revenue from involuntary churn.

Every month, subscription businesses lose thousands of dollars to failed payments that never get recovered. A mid-sized SaaS processing $2M annually with a 5% payment failure rate has $100K at risk. With proper revenue recovery strategies, that's $50-70K waiting to be recaptured.

I've spent seven years optimizing payment systems across subscription businesses. What I've learned: most companies treat failed payments like dead ends. They're not. They're revenue waiting to be recovered.

Quick Answer

Payment retry strategies automatically re-attempt failed transactions at smart intervals, recovering 45-70% of declined payments without bothering customers through timing optimization and customer communication.

What Exactly Is a Payment Retry?

A payment retry is an automated attempt to charge a customer's payment method again after an initial failure, without requiring manual customer intervention.

Here's the scenario: Your customer's credit card gets declined on renewal. Maybe insufficient funds. Maybe a network glitch. Instead of immediately canceling or waiting for them to notice, your system automatically tries again three days later, then seven days after that.

According to Stripe's payment data, a single automated retry recovers approximately 32% of failed transactions. That's nearly one-third of lost revenue, captured without any customer friction.

The difference between naive retries and smart retries is strategy. Naive approaches hammer the same card every 24 hours, triggering fraud alerts. Smart retries use timing logic, failure analysis, and multi-channel approaches to maximize success while minimizing friction.

Why Do Payments Fail?

Understanding failure reasons determines your recovery strategy.

Insufficient funds account for 56% of recurring payment failures—particularly common when customers aren't actively monitoring accounts. Expired or replaced cards cause 18-25% of failures; customers get new cards but forget to update subscription payment methods.

False fraud declines block 15-20% of legitimate transactions, with 56% of U.S. shoppers experiencing false declines in 2023. Network or processor errors create 5-10% of temporary failures that resolve within hours.

The painful reality: only 25% of customers will retry a failed payment, and 39% abandon entirely. The burden of recovery falls on you.

Here's the math that matters: If you're processing $1M in annual subscriptions with a 5% failure rate, that's $50K at risk. Implement smart retry strategies recovering 60% of failures, and you've recaptured $30K annually. Scale that across enterprise volumes, and you hit six figures fast. Beyond immediate recovery, properly handling failed payments plays a crucial role in reducing involuntary churn and increasing customer lifetime value.

Soft Declines vs. Hard Declines: The Critical Distinction

This determines whether retrying will work at all.

Soft declines are temporary failures that may succeed if retried: insufficient funds, daily spending limits reached, network timeouts, or generic "do not honor" codes. Hard declines are permanent failures requiring customer action: stolen/lost cards, closed accounts, invalid card numbers, or expired cards without updater services.

Approximately 70% of initial declines are soft declines, meaning they're recoverable through intelligent retry strategies.

The mistake I see constantly: businesses treating all declines identically. They either retry everything (wasting attempts on hard declines and triggering fees) or retry nothing (leaving money on the table).

Your system needs to parse decline reason codes:

- Code 51 (insufficient funds): Soft decline, retry in 3-5 days

- Code 57 (transaction not permitted): Hard decline, request payment method update immediately

- Code 05 (do not honor): Ambiguous, try 2-3 times with spacing

Smart recovery focuses exclusively on soft declines. That's where your ROI lives.

How to Time Your Payment Retries

Timing determines recovery success. Retry too soon and you hit the same problem. Wait too long and you lose the customer.

The optimal retry schedule:

| Retry Attempt | Timing After Failure | Rationale |

|---|---|---|

| Retry #1 | 1 day | Quick resolution for temporary glitches |

| Retry #2 | 3 days | Allows time for funds to arrive |

| Retry #3 | 7 days | Catches next week's paychecks |

| Retry #4 | 14 days | Aligns with bi-weekly pay cycles |

This schedule aligns with real-world behavior. Most U.S. employees get paid bi-weekly or monthly. Spacing retries 7-14 days apart catches customers when funds are available.

Card network limits matter. Visa and Mastercard recommend not exceeding 15 retry attempts in 30 days, and excessive retries trigger fees. Mastercard charges $0.50 per attempt after 35 tries in a billing cycle.

I recommend 4-6 well-spaced attempts for most subscription businesses. Beyond that, diminishing returns kick in hard. Stripe's default of 8 attempts over 14 days works, but I've found fewer, better-timed attempts yield similar recovery with lower costs.

Customer Communication: The Missing Piece

Technology alone won't save you. Customer communication is equally critical.

Most customers have no idea their payment failed until they lose access. By then, frustration sets in and churn risk skyrockets. When customers are locked out due to payment failure, 62% never return.

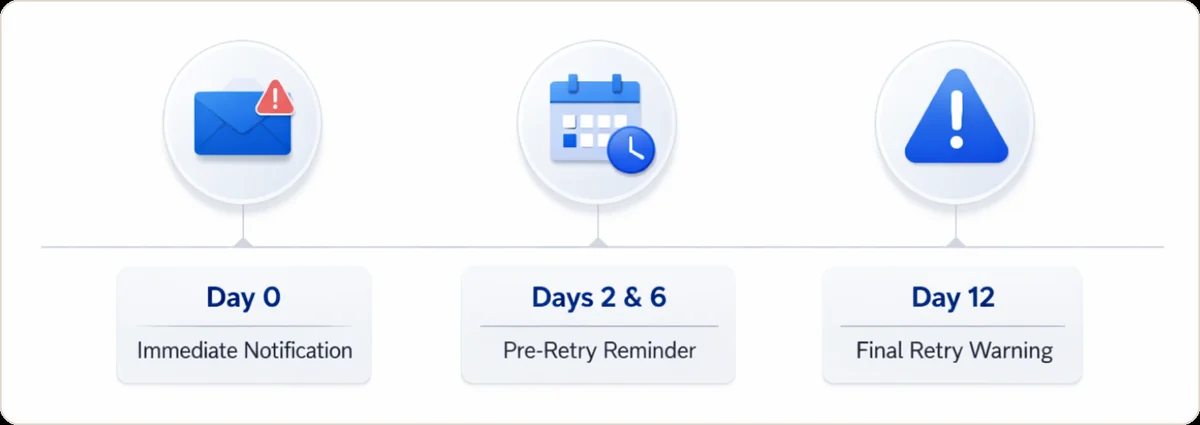

The dunning communication strategy that works:

Day 0 - Immediate failure notification: Email within hours with a helpful tone: "We weren't able to process your payment. No worries—we'll retry automatically in 3 days. Update your payment method here if needed." Include a one-click link to payment settings.

Days 2, 6 - Pre-retry reminders: "Just a heads up—we'll retry your payment tomorrow." Reinforces that you're handling it while giving them a chance to act first.

Day 12 - Final attempt warning: "Last retry coming up on Day 14. Please update your payment method to avoid service interruption." Higher urgency, still empathetic.

Post-failure escalation: Offer a subscription pause instead of immediate cancellation. Give 7 more days to resolve before hard cancel. This approach not only recovers more revenue but also helps with preventing disputes before they escalate to chargebacks, as frustrated customers often file disputes when they feel unfairly charged or locked out.

Alternative Payment Methods and Recovery Channels

Credit cards aren't your only recovery option.

ACH (bank debit) payments have different dynamics: NACHA rules allow resubmission within 180 days for insufficient funds returns. Success rates are often higher on second attempts because bank balances fluctuate more predictably than credit limits. Processing fees are lower, making multiple retries more cost-effective.

I always recommend offering backup payment methods during onboarding. If the primary credit card fails, automatically try the backup card or ACH account before sending dunning emails.

Payment routing optimization is an advanced tactic most businesses miss. If you use multiple payment processors, route failed transactions through an alternate gateway on retry. Trying a different processor can instantly recover about 8% of failures that would otherwise remain declined.

Network tokenization and account updater services work behind the scenes to prevent failures: Visa Account Updater and Mastercard Automatic Billing Updater automatically refresh card numbers when customers receive new cards. This turns what would be hard declines into seamless transactions.

The Realistic Revenue Impact

Let me show you the math with a real scenario.

Example: Mid-sized SaaS company

- Monthly recurring revenue: $175K

- Annual revenue: $2.1M

- Payment failure rate: 5%

- Failed payment volume: $105K annually

- Current recovery (basic retries): 30%

- Revenue recovered currently: $31.5K

After implementing smart retry strategies:

- New recovery rate: 60%

- Revenue recovered: $63K

- Net improvement: $31.5K annually

Scale that over three years: $94,500 in recovered revenue that would have been written off as churn.

For growing subscription businesses processing $3-5M annually, comprehensive retry strategies can recover $200K-$400K over three years—our title's $347K figure represents the mid-range for companies in this bracket who implement the full framework.

Basic vs. Smart Retry Strategies

| Feature | Basic Retry | Smart Retry Strategy |

|---|---|---|

| Decline Analysis | Retries all failures equally | Differentiates soft vs. hard declines |

| Timing Logic | Fixed schedule (e.g., daily) | Dynamic, data-driven scheduling |

| Retry Limit | Often excessive (10+ attempts) | Optimized (4-6 attempts) |

| Customer Communication | Generic or none | Personalized dunning cadence |

| Multi-Channel | Single payment method | Backup methods + routing |

| Recovery Rate | 25-35% | 45-70% |

Common Implementation Mistakes

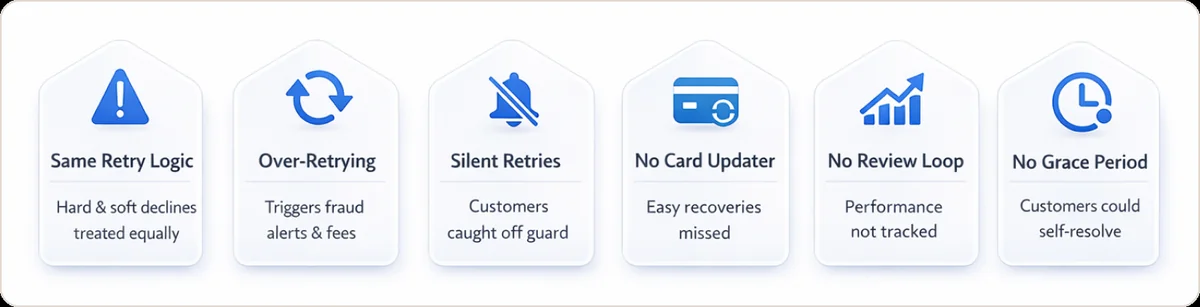

Treating all declines the same: Retrying hard declines wastes money and annoys customers. Parse reason codes and route accordingly.

Retrying too aggressively: Seven attempts in three days trigger fraud alerts and incur network fees. Space them intelligently.

No customer communication: Silent retries confuse customers when charges appear later, or access gets cut off unexpectedly.

Ignoring account updater services: Expired cards are the easiest failures to prevent. Integrate updater tools into your subscription billing workflows.

Never reviewing performance: What works for one customer segment may fail for another. Establish key performance metrics and track them monthly.

Immediate cancellation after final failure: Offer a grace period or pause option. Many customers will self-resolve if given time.

Start Recovering Lost Revenue Today

Failed payments aren't a cost of doing business. They're recoverable revenue waiting for the right strategy.

The framework is straightforward: differentiate soft and hard declines, implement intelligent retry timing based on customer pay cycles, enable multi-channel recovery with backup payment methods, communicate proactively throughout the retry process, and monitor performance metrics continuously.

Most businesses recover an additional 15-30% of failed payments within the first 90 days of implementing these strategies. That's predictable, measurable revenue protection. For more comprehensive tactics on recovering lost revenue, explore our guide on failed payment recovery strategies.

Start with your billing platform's retry settings. Configure a proper schedule. Turn on dunning emails. That alone will move the needle. Then layer in account updater services, analyze your decline reason codes, and test different communication cadences.

The revenue is already there—you just need better systems to capture it.

Ready to Protect Your Revenue?

Beast Insights helps subscription businesses build intelligent payment recovery systems that reduce involuntary churn and protect revenue. Our payment optimization consultations identify your specific failure patterns and design custom retry workflows.

Schedule a payment strategy consultation →

FAQ: Payment Retry Strategies

What is a payment retry?

A payment retry is an automated re-attempt to charge a customer's payment method after an initial decline, using optimized timing to recover failed transactions without manual intervention. Most systems attempt 4-6 retries over 14-21 days for maximum recovery.

How many times should you retry a failed payment?

Most subscription businesses should attempt 4-6 retries over 14-21 days, balancing recovery potential against network fees. Stripe recommends not exceeding 8 attempts in 14 days, while I've found 4-6 well-timed attempts offer the best cost-to-recovery ratio.

What's the difference between soft and hard declines?

Soft declines are temporary failures like insufficient funds that may succeed on retry, accounting for 70% of initial declines. Hard declines are permanent issues like closed accounts that require customer action to resolve and should not be retried.

When should you retry a declined payment?

Retry soft declines after 1 day, 3 days, 7 days, and 14 days to align with customer pay cycles. Never retry hard declines without first obtaining updated payment information from the customer to avoid wasted attempts and network fees.

How much revenue can smart payment retries recover?

Smart retry strategies recover 45-70% of soft decline failures, compared to 25-35% for basic approaches. For subscription businesses processing $2-5M annually, this represents $30K-$100K+ in annual recovered revenue that would otherwise be lost to involuntary churn.

What is dunning management?

Dunning management combines automated payment retry attempts with proactive customer communication via email and SMS to maximize recovery. Effective dunning reduces involuntary churn by 15-20% while maintaining positive customer relationships through transparent, helpful messaging.