Card Account Updater in 2026: Recovering $180K from Failed Recurring Payments

Card account updater technology automatically syncs expired credit card details, preventing failed recurring payments. Proven ROI of 1,600%+ for subscription businesses through reduced involuntary churn.

A SaaS founder called at 11 PM after their monthly renewal batch processed. Twenty-three percent of subscribers, loyal customers who'd been with them for years, were flagged as "payment failed." The worst part? These weren't deliberate cancellations. They were victims of involuntary churn: customers lost due to outdated credit card information.

Card account updater services were implemented for this company. Within 60 days, they recovered $180,000 in what would have been lost annual recurring revenue. The customer experience was completely invisible. No angry emails, no "update your payment method" notifications, just seamless continuity.

If you're running a subscription business and seeing decline rates above 10%, this technology isn't optional anymore. According to PYMNTS research on subscription churn from failed payments, failed payments cause 50% of involuntary churn, with 27% of subscribers likely to cancel due to avoidable issues and manual 'update your info' prompts often accelerate it.

What Is a Card Account Updater?

A card account updater automatically syncs new credit card details from issuing banks to your payment system when cards expire or change, preventing failed recurring payments without customer action. The service works through Visa Account Updater (VAU), Mastercard Automatic Billing Updater (ABU), and similar networks from American Express and Discover.

Mastercard's Automatic Billing Updater (ABU) helps reduce declines from outdated cards. Industry data shows 15% of recurring credit card payments fail, often from expired or invalid info, accounting for up to 50% of subscription churn.

The problem compounds quickly. When a subscription payment fails, you lose the immediate monthly recurring revenue, the future lifetime value of that customer, and the marketing dollars spent acquiring them. For a mid-sized SaaS company with $500K in MRR and a typical 13-18% decline rate, that's potentially $65,000-$90,000 monthly in preventable payment failures.

The psychological dimension matters equally. When customers receive a failed payment notification, they enter a "re-evaluation moment." That previously passive, satisfied customer now asks: "Do I still need this? Is finding my wallet worth it?" Research consistently shows most decide it isn't, which is why understanding involuntary churn should be a priority for any subscription business.

How Card Account Updater Works: The Five-Step Process

Your payment processor identifies cards approaching expiration (typically 5-7 days before billing) or cards that recently returned specific decline codes like "expired card" or "invalid card number." The system flags these for update requests and initiates a secure multi-party communication flow.

1. System Identifies Expiring Cards

Your payment gateway scans stored payment methods for upcoming expirations or recent soft declines that indicate outdated information.

2. Network Handshake

Your processor sends an encrypted inquiry to the appropriate card network. Visa uses Account Updater for Visa cards, Mastercard utilizes Automatic Billing Updater for Mastercard, and equivalent services exist for Amex and Discover.

3. Bank Verification

The card network routes the request to the issuing bank (Chase, Bank of America, Capital One, etc.). The bank's system identifies whether the account has new details: updated expiration dates, new card numbers due to fraud replacement, or account closure status.

4. Secure Data Return

Updated information travels back through the network to your acquirer, encrypted end-to-end using PCI DSS 4.0 compliant protocols. This entire exchange happens without exposing raw card numbers.

5. Token Synchronization

Your payment vault automatically updates the tokenized card reference. The existing customer_token or payment_method_id remains the same. Only the underlying card data changes. Your next billing attempt uses the refreshed information without requiring code changes or customer interaction.

The entire process completes in 24-72 hours for batch systems, or in real-time (under 3 seconds) for modern API-based implementations. This differs fundamentally from payment retry strategies, which attempt to re-process existing card data. Credit card updater services fetch entirely new card details before the retry even happens.

Real-Time vs. Batch: Which Model Fits Your Business?

When consulting with revenue operations teams, choosing between real-time and batch processing dramatically impacts authorization rates. The most sophisticated payment architectures use both.

| Feature | Batch Account Updater | Real-Time Account Updater |

|---|---|---|

| Update Timing | Proactive; scheduled intervals (daily/weekly) before billing cycles | Reactive; triggered during or immediately after transaction failure |

| Best Use Case | High-volume subscriptions with fixed monthly billing dates | On-demand billing, usage-based pricing, or high-frequency charges |

| Network Support | All four major networks (Visa, Mastercard, Amex, Discover) | Primarily Visa and Mastercard; Amex varies by processor |

| Security Protocol | SFTP/PGP file transfers; batch processing | API-based; integrated via webhooks in standard payment flow |

| Recovery Speed | Prevents first-attempt failures; portfolio-wide refreshes | Rescues failed transactions mid-cycle; reduces dunning sequences |

If you're running a SaaS business with 10,000 subscribers billed on the 1st of each month, a batch process running on the 25th-27th ensures maximum coverage. But if you also offer annual upgrades or usage overages that bill unpredictably, real-time updates catch those edge cases. This hybrid approach is what gets recommended when conducting approval rate drop analysis for clients.

The Real ROI: How Much Revenue Can You Recover?

The financial impact extends beyond the immediate lost transaction. According to Stripe's published case study on Postmates' revenue recovery, when Postmates integrated card updater technology, they achieved a 1.72% increase in authorization rates. This resulted in $60 million in recovered revenue over 18 months.

For smaller businesses, the math is equally compelling. A B2B software company had 4% of its $100K MRR failing each month due to card issues. Before implementing credit card account updater technology, they recovered about 25% through manual dunning emails. After implementation, their recovery rate jumped to 35%.

Their annualized impact:

- Additional recovered revenue: $48,000/year

- Saved customer support hours: 120 hours/year ($6,000 value)

- Avoided customer acquisition cost to replace churned customers: $84,000/year (assuming $350 CAC and 20 customers saved monthly)

- Total annual benefit: $138,000 on a service costing approximately $8,000/year

- ROI: 1,625%

When you factor in the extended customer lifetime value and expansion revenue potential from customers who would have churned, the numbers become even more significant.

Which Payment Processors Offer the Best Integration?

Card account updater systems have been implemented across every major payment gateway. Here's an assessment of who excels where:

| Processor | Network Coverage | Real-Time Support | Batch Processing | Best For |

|---|---|---|---|---|

| Stripe | Visa, Mastercard, Amex, Discover | Yes (automatic) | Yes | SaaS $50K+ MRR; developer-friendly APIs |

| Adyen | Visa, Mastercard, Amex | Yes (configurable) | Yes | Global enterprises; multi-currency |

| Braintree | Visa, Mastercard | Yes (PayPal ecosystem) | Limited | Businesses using PayPal infrastructure |

| Recurly | Visa, Mastercard | Yes | Yes | Subscription-focused; integrated dunning |

| Authorize.Net | Visa, Mastercard | No | Yes | Traditional SMBs; stability over innovation |

Stripe dominates developer experience. Their implementation requires adding a single parameter (setup_future_usage: 'off_session') to your payment intent API call, and updates happen automatically via their network tokens system.

Adyen excels for enterprises managing multiple acquirer relationships across continents. Their network token feature goes beyond basic card updater by replacing static card numbers with dynamic tokens that update automatically across network changes.

Recurly is ideal for businesses needing card updater as part of holistic churn management. They bundle it with intelligent dunning, subscription analytics, and revenue recognition.

Pricing Reality

Stripe includes credit card updater services free with standard transaction fees. Standalone services typically charge $0.01-$0.05 per successful update, or $100-$500 monthly for batch processing. When you compare this to the cost of recovering failed payments manually or the lifetime value of retained customers, the ROI consistently exceeds 1,000%.

Technical Implementation: What Developers Need to Know

For API-first processors like Stripe, Adyen, or Square, implementation takes 1-2 hours. You need to ensure payment methods are created with off_session usage enabled, and the processor handles all card data within their PCI scope.

For traditional gateways like Authorize.Net or First Data, expect 1-2 weeks. You'll configure batch file downloads via SFTP, map updated tokens to customer records, and secure file transfers to maintain PCI DSS 4.0 compliance.

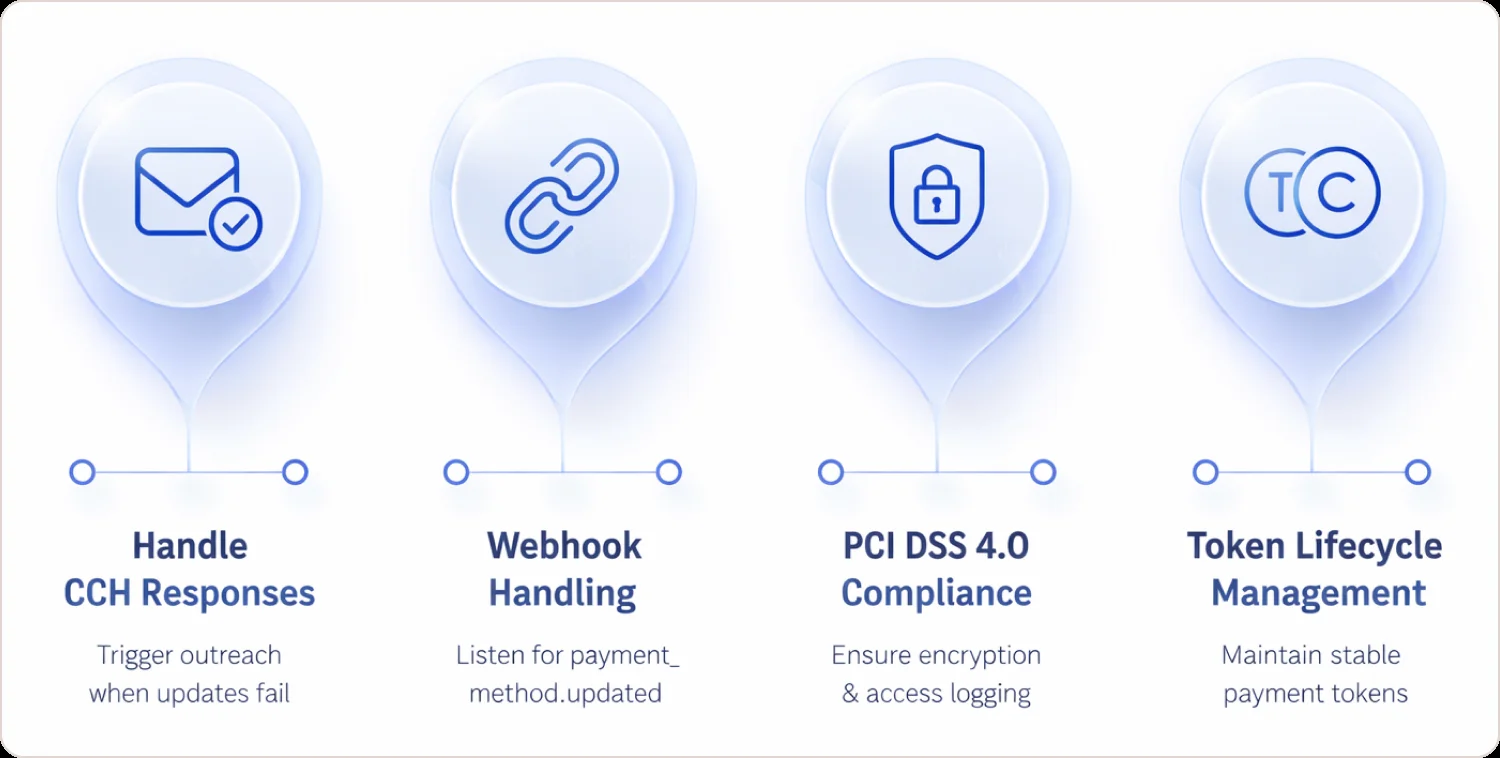

Four Critical Developer Considerations

1. Handle "Contact Cardholder" (CCH) Responses

Not every update request succeeds. Banks return CCH codes when cards are closed or customers need to provide new details manually. Your system should trigger gentle outreach in these cases, not assume the update succeeded. This overlaps with proper credit card decline code handling.

2. Webhook Handling for Real-Time Updates

Modern processors send payment_method.updated webhooks when card details change. Your backend should listen for these events and update subscription records accordingly. Don't rely solely on pre-billing checks.

3. PCI DSS 4.0 Compliance

As of 2025, any system storing or transmitting cardholder data must meet the latest PCI standards with stricter encryption and access logging requirements. Using a processor's hosted updater keeps you out of direct PCI scope, which is why gateway compliance monitoring becomes increasingly important.

4. Token Lifecycle Management

Even though the underlying card changes, your customer_id or payment_token reference should remain stable. Avoid creating new tokens on updates. This breaks subscription continuity and analytics tracking.

The Psychology of Transparent Automation

The old approach was complete silence. The update happens invisibly, and customers never know. The emerging 2026 standard is transparent automation.

When someone receives an "Update Your Payment Method" email, they enter a re-evaluation moment. That previously passive, satisfied customer now questions the service value against the effort of finding their wallet. Industry data shows 60% conclude it isn't worth it.

But there's a trust opportunity when you handle updates well. After a card is successfully updated, display a brief message in the customer's account dashboard: "Your card ending in 4242 was recently replaced. We've updated your billing information to keep your service active."

This isn't asking customers to do anything. It's demonstrating proactive care. Think of it like Amazon's "Your package has shipped" emails. You didn't request an update, but you're glad to know things are moving smoothly.

The brands implementing this approach report improved customer satisfaction, specifically around billing transparency, with zero increase in voluntary cancellations. It's about reducing friction while building trust, which is why understanding the full context of card scheme compliance matters for the complete customer experience.

Why This Technology Matters in 2026

Eight years have been spent helping subscription businesses protect revenue streams. Card account updater isn't a "nice-to-have" feature anymore. It's foundational infrastructure for sustainable subscription growth.

The businesses winning in the subscription economy aren't just acquiring customers faster. They're keeping them longer by eliminating every friction point in the payment experience. When a customer's card expires and your system seamlessly updates it before they notice, you're not just preventing a failed transaction. You're extending a relationship worth thousands in lifetime value.

The reality:

- 40-53% of churn is involuntary and preventable with credit card updater services

- 60% of customers cancel after one failed payment if forced to update manually

- Implementation takes 1-4 weeks with modern payment infrastructure

- ROI exceeds 1,600% for typical SaaS businesses when factoring in saved CAC and extended LTV

According to Gartner's research on subscription billing, modern solutions with automated updates reduce churn and boost retention in competitive markets. When operating in an environment where acquisition costs are rising, retention becomes the key growth driver.

If you're experiencing decline rates above 10%, seeing involuntary churn eat into growth metrics, or tired of sending dunning emails that trigger cancellations, it's time to implement card account updater as part of your comprehensive failed payment recovery strategy.

The future of subscription revenue isn't about adding more customers. It's about keeping the ones you already have. Start there.

Frequently Asked Questions

What is a card account updater?

An automated system that syncs new credit card details from issuing banks to merchant payment vaults when cards expire, get replaced, or change. It prevents failed recurring payments without customer action.

How does card account updater work?

Your payment processor identifies expiring cards, sends secure requests to card networks (Visa/Mastercard), networks query issuing banks, banks return new card details, and your vault automatically updates tokenized references without customer involvement.

How much does Card Account Updater cost?

Stripe includes it free. Standalone services charge $0.01-$0.05 per successful update or $100-$500 monthly for batch processing. ROI typically exceeds 1,000% due to recovered revenue and reduced support costs.

What's the difference between Visa Account Updater and Mastercard ABU?

Both provide the same function. Visa Account Updater (VAU) covers Visa cards globally; Mastercard Automatic Billing Updater (ABU) handles Mastercard. Both deliver updated card numbers, expiration dates, and account status through secure network protocols.

Why do recurring payments fail?

15% of failures stem from outdated card information. Other causes include insufficient funds (40%), fraud blocks (12%), and technical issues (8%). Card account updater specifically prevents the outdated card category.

Batch vs real-time card updater: which is better?

Batch updater proactively refreshes cards on schedules (ideal for fixed monthly billing). Real-time updater fetches updates during transaction failures (ideal for on-demand billing). Best practice uses both in a hybrid model.

How to reduce involuntary churn?

Implement card account updater to prevent 40-50% of involuntary churn from card issues. Combine with smart retry logic, dunning management, and network tokenization for comprehensive revenue recovery.