Intelligent Payment Routing: Smart, Dynamic & Static

Intelligent payment routing beats fixed rules only when you measure per-acquirer approval rates, decline codes, and cost in near real time. Here is how dynamic and cascading routing work, and why the performance signal feeding them decides whether routing lifts approvals or leaks revenue.

Intelligent payment routing sends each transaction to the acquirer most likely to approve it at the lowest cost. It decides per payment instead of following one fixed path. The catch: it only beats static routing when you can measure per-acquirer approval rates, decline reasons, and cost in near real time. Routing is a data problem before it is a config switch.

What is intelligent payment routing (and why it beats fixed rules)

Intelligent payment routing selects the best acquirer per transaction in real time. It bases that choice on BIN range, issuer relationship, and geography. A BIN, or bank identification number, is the first digits of a card number that identify the issuer. Static routing instead sends everything to one acquirer regardless of fit. Every acquirer approves differently by issuer, geography, and card type. Matching each payment to the right path is where the lift lives.

Fixed rules leave money on the table for a structural reason. A single-PSP setup routes all transactions to the same acquirer with no fallback. A PSP, or payment service provider, connects a merchant to acquirers and card networks. That setup cannot exploit the fact that approval rates vary by 10 to 25 percentage points across acquirers for the same BIN. Intelligent routing evaluates each payment against configurable conditions built from observed performance data. This is only possible if that performance data exists. If you are still mapping how routing itself works, start with our primer on what payment routing is.

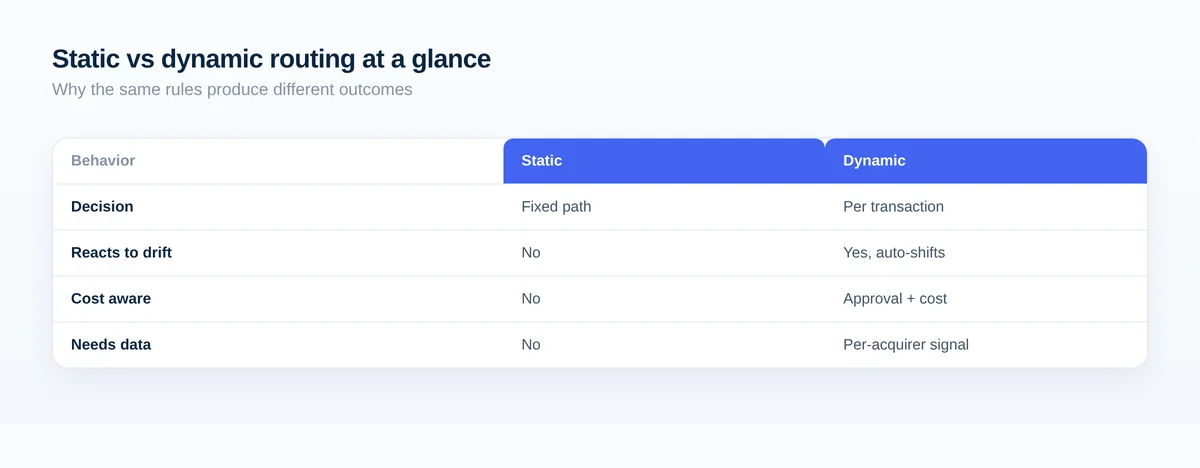

Static vs dynamic payment routing: the core difference

Static routing sends every transaction through a fixed, pre-configured acquirer path. Dynamic payment routing makes a fresh decision on each transaction. It selects the acquirer with the highest approval probability based on card type, issuer, geography, and live performance data. The difference is not the rules. The difference is whether a live signal or a stale assumption drives them.

Static rules are based on patterns that were true when they were written. They inevitably become outdated. A static rule will not recognize a processor's performance drop and reroute unless another rule adjusts traffic on real-time changes. Static setups can therefore see approval-rate drops of up to 5 to 10 percent when card networks change authorization rules. They cannot adapt. Dynamic routing responds in real time. Its routing logic updates continuously on live approval-rate data. The freshness of that signal bounds its quality.

| Dimension | Static routing | Dynamic / intelligent routing |

|---|---|---|

| Decision basis | Fixed path for every transaction | Fresh per-transaction decision on live data |

| Reacts to drift | No, keeps sending to a struggling acquirer | Yes, shifts volume to a better performer |

| Cost awareness | None, one fixed rate | Evaluates approval and cost per corridor |

| Data requirement | None beyond initial config | Per-acquirer, per-BIN approval-rate signal |

| Failure mode | Accepts declines, revenue loss unnoticed for months | Bounded by signal freshness and granularity |

The honest framing matters here: dynamic beats static only with data. Without unified PSP data, a performance trend can take days to spot. With it, the adjustment takes minutes. The routing decision itself runs in under 100 milliseconds against live signals. Static routing, by contrast, keeps sending traffic to a struggling processor. It quietly accepts those declines.

Smart routing and cascading payments: retrying declines across acquirers

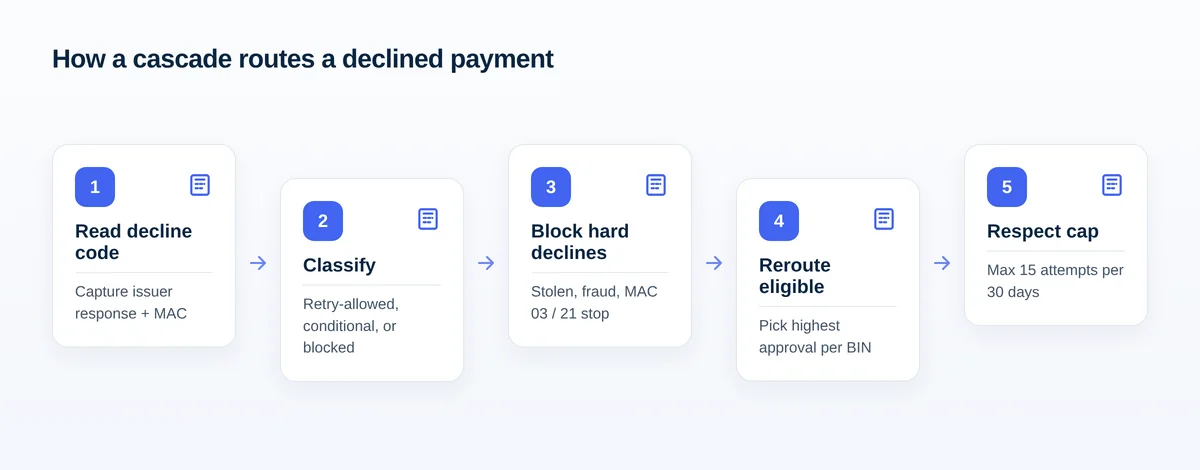

Payment cascading retries a failed authorization across an alternative acquirer or processor. It runs under explicit decision rules with deterministic state. It is not a static ordered list. A well-tuned cascade sends to the acquirer most likely to approve that specific transaction. This requires the rolling approval rate per BIN per acquirer over the last 7, 30, and 90 days.

Decline reasons gate cascading, not blind retries. A cascade engine classifies each decline into retry-allowed, retry-conditional, or retry-blocked before any attempt. Retry-allowed covers issuer-side noise such as temporary unavailability or a generic decline. Retry-blocked codes such as lost-or-stolen, suspected fraud, and closed accounts must not be re-routed. Done right, cascade logic recovers an additional 8 to 15 percent of declined volume. Real-world cascade attempts approve in the 25 to 45 percent range.

Network rules set a hard ceiling. As of 2026, Visa and Mastercard cap retries at 15 attempts per card per merchant within a rolling 30-day window. Excessive Mastercard retries incur $1.00 per transaction in the first month, escalating to $2.00 after. Cross-PSP retries add value precisely because many declines stem from an issuer-acquirer combination rather than the card itself. They typically add 2 to 5 percentage points of recovery beyond same-PSP retries. Running several acquirers well is its own discipline. We cover it in our guide to a multi-acquirer strategy.

The signals that drive good routing decisions

Good routing conditions on three signals measured per acquirer. Those signals are approval rate (by BIN, issuer, and geography), classified decline reason codes, and net processing cost. Approval rate by BIN per acquirer is the primary observability metric that routing weights sit on. Watching it shift week over week reveals issuer behavior changes before they become a revenue problem.

Cost is a first-class signal, not an afterthought. Dynamic routing evaluates both approval probability and processing cost on every transaction. It selects the acquirer with the strongest issuer relationships in that market and the most competitive fee for that corridor. True cost is composite. Interchange, scheme fees, authentication costs, and fraud losses all contribute to cost per successful transaction. Routing cost can only be measured net, not from headline pricing.

- Approval rate per acquirer, segmented by BIN, issuer, card network, and geography, tracked as a rolling window over 7, 30, and 90 days.

- Decline reason codes classified into retry-allowed, retry-conditional, and retry-blocked buckets, including Mastercard Merchant Advice Codes that gate whether a retry is permitted at all.

- Net cost per successful authorization, accounting for interchange, scheme fees, authentication, and fraud losses, compared per route rather than by advertised price.

How intelligent routing lifts approval rates and recovers failed payments

The upside is a measurable gap. General e-commerce card-not-present transactions typically see authorization rates between 85 and 92 percent. Optimized global merchants using tokenization and smart routing reach 91 to 96 percent or higher. That band is the headroom static routing leaves on the table. It is only reachable with measured, per-segment routing.

The recovery numbers stack up. Rerouting on a general decline recovers 20 to 25 percent of transactions that would otherwise be permanently lost. Up to 25 percent of card declines are false positives. Payment cascading across acquirer fallbacks delivers an average 14.8 percent LTV lift. LTV, or lifetime value, is the total revenue a merchant expects from a customer. Routing each transaction to the most effective provider typically lifts overall approval rates by 10 to 15 percent. The stakes are concrete: for a business processing $1 billion annually, a 1 percent increase in authorization rate equals $10 million in recovered revenue.

Cross-border routing is where segmentation pays off most. International cards typically run 5 to 15 percentage points lower than domestic rates due to extra fraud checks. Switching to local acquiring has delivered an average LTV improvement of up to 17.9 percent across cross-border corridors. Knowing when local acquiring will help is a measurement question. We unpack it in our comparison of cross-border vs local acquiring.

Routing pitfalls for subscription merchants

For subscription merchants and businesses, the biggest routing pitfall is treating retries as a schedule instead of a signal. Soft declines account for 70 to 90 percent of all declines. A well-targeted retry strategy recovers 40 to 70 percent of them. This works only if you classify decline reasons rather than retry blindly against a fixed cadence.

The second pitfall is ignoring decline-code signals and paying for it. Mastercard MAC 03 (do not retry) and MAC 21 (stop all retries) demand an immediate stop. A MAC, or merchant advice code, tells the merchant why a transaction was declined and whether to retry. Retrying anyway triggers excess authorization fees. Those fees reached $0.50 per transaction as of January 2025, up from $0.10 in 2022. Most billing systems receive MAC data in authorization responses without routing it to any retry logic. At 10,000 monthly declines and a 20 percent violation rate, that is $2,000 to $10,000 a month in avoidable fees.

The third pitfall is compliance drift. Every routing decision affects approval rate, cost, and compliance friction at once. Visa's VAMP merchant threshold dropped from 2.20 percent to 1.50 percent effective April 1, 2026. VAMP, or the Visa Acquirer Monitoring Program, flags acquirers and merchants with excessive fraud and disputes. Over-blocking backfires: declining legitimate transactions shrinks the denominator without reducing the numerator. Approval-preserving routing is now a compliance requirement, not just an optimization.

Measuring routing performance before you optimize

Before optimizing routing, instrument performance at a segmented, per-acquirer granularity rather than in aggregate. Aggregate authorization rate hides where routing is failing. A 92 percent overall rate can mask an 85 percent rate on a single acquirer for EU-issued cards. That points to a routing, rules, or issuer-messaging problem you cannot fix without the segment view.

Smart routing has a data floor. It needs at least two active PSPs and roughly 10,000 transactions per month to surface meaningful processor-level patterns. The measurement must be near real time to change outcomes. The most sophisticated merchants track variance and drift, not just headline averages. An acquirer that approved 94 percent of a BIN last quarter and 71 percent this week has changed. Only near-real-time measurement catches it.

- Pull approval-rate data segmented by issuing country, card network, acquirer, and transaction type (first-time vs recurring).

- Track approval rate by BIN per acquirer as a rolling 7, 30, and 90-day window to catch drift early.

- Classify every decline into retry-allowed, retry-conditional, or retry-blocked using decline codes and Merchant Advice Codes.

- Route MAC data from authorization responses into your retry logic to avoid do-not-retry fees.

- Measure net cost per successful authorization, including interchange, scheme, authentication, and fraud costs.

- Monitor chargeback ratio by acquirer, region, and currency against tightening VAMP thresholds.

- Confirm you have at least two active PSPs and enough monthly volume to surface processor-level patterns.

Frequently Asked Questions

What is intelligent payment routing?

Intelligent payment routing selects the best acquirer per transaction in real time, based on BIN range, issuer relationship, and geography, instead of sending every payment through one fixed path. It evaluates each payment against conditions built from observed performance data, so its quality depends entirely on the approval-rate signal feeding it.

What is the difference between static and dynamic payment routing?

Static routing sends every transaction through a fixed, pre-configured acquirer path. Dynamic payment routing makes a fresh decision on each transaction, choosing the acquirer with the highest approval probability from card type, issuer, geography, and live performance data. Dynamic beats static only when a live signal replaces the stale, hard-coded assumption.

How do smart routing and cascading payments recover declines?

Cascading retries a failed authorization across an alternative acquirer under explicit decline-code rules. It classifies each decline as retry-allowed, retry-conditional, or retry-blocked, then reroutes only eligible ones. Well-tuned cascade logic recovers an additional 8 to 15 percent of declined volume, with cross-PSP retries adding 2 to 5 points beyond same-PSP retries.

How much can intelligent routing lift approval rates?

Routing each transaction to the most effective provider typically lifts overall approval rates by 10 to 15 percent, and rerouting general declines recovers 20 to 25 percent of otherwise-lost transactions. For a business processing $1 billion annually, each 1 percent approval-rate gain equals about $10 million in recovered revenue.

What data do I need before optimizing routing?

You need per-acquirer approval rate segmented by BIN, issuer, geography, and transaction type, classified decline codes, and net cost per successful authorization, measured in near real time. Smart routing needs at least two active PSPs and roughly 10,000 monthly transactions to surface meaningful processor-level patterns.