Issuer Declined MCC: Why Declines Hit by Category

An "Issuer Declined MCC" means the bank refused a charge because of your merchant category code, not the card. Here is how to isolate MCC and issuer-rule declines from card-level ones, and which levers, routing, MID structure, retries, actually move them.

An "issuer declined mcc" response is not a card problem. It means the cardholder's bank refused the charge because of your merchant category code (MCC). The MCC is the four-digit number that classifies your business type. Either the bank blocks that category, or your account was set up with the wrong MCC. You can fix both, but not by retrying the card.

That distinction matters. Teams routinely troubleshoot their own checkout when the decision actually sits with the customer's bank. issuer-decline patterns are the first fork in isolating an MCC or issuer-rule block from a card-level or gateway fault. This guide walks the diagnostic. It covers what an MCC decline looks like and how to separate it from generic credit-card-decline-code noise. It also covers which levers actually move it: MID structure, routing, and retries. Getting this right is the difference between real failed-payment-recovery and burning reattempt fees.

What an MCC is and why issuers score declines by category

A merchant category code is a four-digit number. The card networks assign it to classify the goods or services a business sells. It is an implementation of the ISO 18245 standard used by Visa, Mastercard, and Amex. Businesses cannot pick their own MCC. The acquirer assigns it, though you can request a specific code if you qualify.

Declines cluster by category because issuers use the MCC directly in authorization logic. At authorization the transaction carries your MCC. The issuer checks that code against the rules configured on the card before the purchase clears. If the MCC is not permitted, the issuer declines the charge in real time. This happens in milliseconds, before any money moves. Banks can restrict a card from certain business types or allow it only at certain ones. Acquirers and networks also use the MCC for activity tracking, reporting, and risk management. So the code you carry shapes how every issuer scores you.

How to tell an MCC/issuer-rule decline from a card-level decline

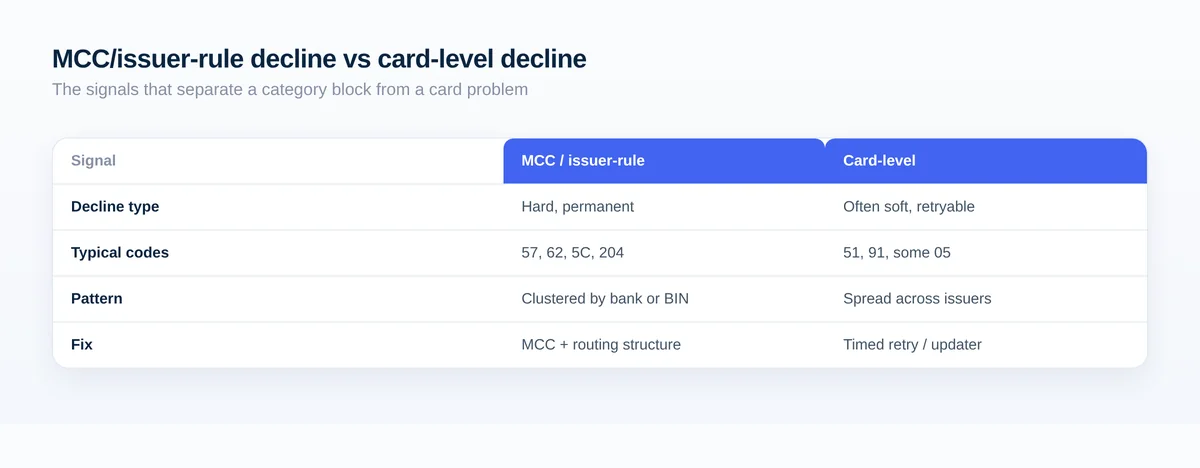

The fastest tell is soft versus hard. A soft decline is a temporary refusal that may succeed on retry. Examples include insufficient funds, an address (AVS) or security-code (CVV) mismatch, and velocity limits. A hard decline is permanent. Never retry it with the same credentials. MCC-related declines are always hard. The block persists until either the card's permissions or your MCC changes.

That single split is the highest-leverage diagnostic step. About 60 to 70% of soft declines are recoverable with the right retry logic and timing. Retrying a hard MCC block only wastes attempts and lowers your authorization rate. The signature of an MCC decline is a hard decline that repeats on the same card, same amount, and same merchant. It repeats regardless of the cardholder's balance.

Visa now makes this easier to read. Effective April 11, 2025, Visa returns code 5C ("transaction not supported or blocked by the issuer"). It applies to all declines due to issuer rules for a specific card range or bank identification number (BIN). That code is a direct signal that the decline is issuer-rule or BIN driven rather than card-level. Code 9G, by contrast, means the cardholder set the block via a card-control app. Do not retry that one.

High-scrutiny MCCs that draw disproportionate issuer attention

Some categories draw blanket scrutiny. Networks designate certain MCCs as high integrity risk and maintain special registration for them. Those industries generate the highest levels of cardholder disputes. That scrutiny compresses approval rates for the whole category, not just the individual merchant.

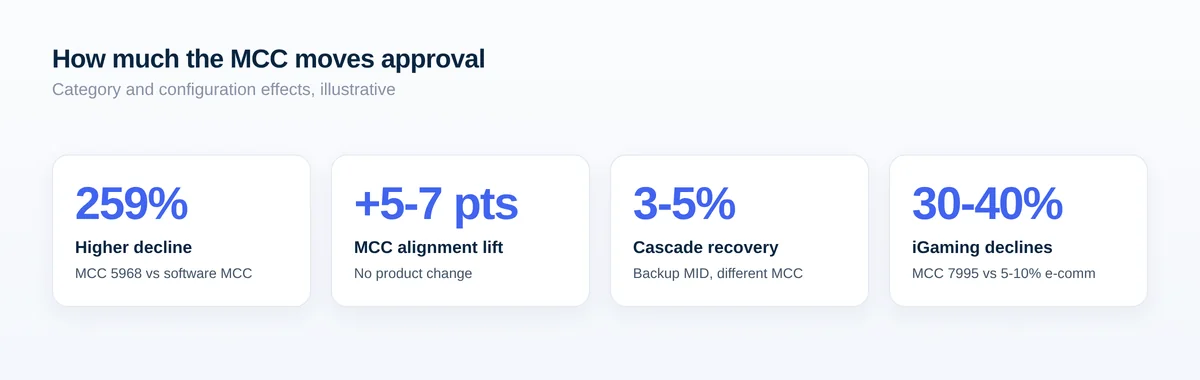

The magnitude is large. FlexPay reports a transaction under MCC 5968 (direct marketing and continuity/subscription) is 259% more likely to decline than the same transaction under MCC 5734 (computer software stores). Many issuers blanket-block certain codes. MCC 5967 (adult entertainment), MCC 5968 (subscription/direct marketing), and MCC 5993 (tobacco) show up as issuer-clustered declines rather than random card-level ones.

Visa formalizes this in the Visa Integrity Risk Program (VIRP), effective May 1, 2023. VIRP tiers high-integrity-risk categories. Tier 1 (highest) includes MCC 5967 (adult content), 7273 (dating), 7995 (gambling), and 5122/5912 (pharmacies). Tier 2 covers crypto (6051, 6012), cyberlockers (4816), and games of skill (5816). Tier 3 covers 6211, 5966, 5968, and 5993.

| MCC | Category | Signal | Diagnostic note |

|---|---|---|---|

| 5967 | Adult entertainment | VIRP Tier 1; blanket-blocked by many issuers | Expect issuer-clustered hard declines, not card-level |

| 7995 | Gambling / betting | VIRP Tier 1; ~30-40% deposit declines | Approval swings by issuer geography and rail |

| 5968 | Subscription / direct marketing | VIRP Tier 3; 259% higher decline vs software | Classic subscription-merchant MCC exposure |

| 6051 / 6012 | Crypto on-ramps | VIRP Tier 2; Special Condition Code 7 required | Miscoding here risks network penalties |

| 5993 | Tobacco | VIRP Tier 3; blanket-blocked by many issuers | Cross-border card-absent draws extra scrutiny |

iGaming (MCC 7995) is the sharpest illustration. About 30 to 40% of card deposits get declined versus 5 to 10% in regular e-commerce. Within those declines, issuers with blanket anti-gambling policies account for 10 to 20%. Do Not Honor (code 05) makes up another 25 to 35%.

Reading the decline: MCC vs decline code vs issuer patterns

You have to read three things together: the raw error, the network decline code, and the issuer pattern across transactions. An MCC-driven decline often surfaces as an "Issuer Declined MCC" message. It can also surface as a 204 error code in gateway logs. That 204 indicates a hard decline by the issuer specifically because of the MCC. That 204 maps to decline code 57 (transaction not permitted).

Code 57 means the card cannot be used for this type of transaction or at this type of merchant. The issuer sets the restriction and ties it to the card product, not the balance. It is a hard decline. Do not retry. Recurring code 57 (and code 62, restricted card) signals card restrictions tied to your industry classification. That is why high-scrutiny merchants hit both far more often.

The trap is code 05, Do Not Honor. It is a generic catch-all that hides the real reason. It is the single highest-volume decline code, accounting for 30 to 40% of all declines. Codes 05 and 51 together are about 76% of declined volume. So you must isolate category and issuer-driven declines from that large 05 bucket before you can act. Code 57 tells you it is a permission restriction. Code 05 tells you nothing, until you segment it by bank.

Networks group codes to help. Visa buckets responses into categories. Category 1 means never approve, do not reattempt. Category 2 means cannot approve now, wait and retry. Category 3 means fix the data and retry. Mastercard consolidates into 79 (Lifecycle), 82 (Policy), and 83 (Security). Code 82 groups the policy-driven codes like 57 and 62 that flag MCC and merchant-type restrictions.

Diagnosing MCC declines by issuer, BIN, and gateway/MID

The aggregate auth rate hides the answer. What matters is performance by segment. Say your overall rate is 92% but falls to 85% on one acquirer for EU-issued cards. The failure point is likely routing, rules, or issuer messaging, not the card. A decline rate concentrated on one BIN points to an issuer-specific policy.

So the workflow is to break declines down below the top line. Pull all declines and group them by decline code. Identify the top five by volume and research each. Then check whether declines concentrate on specific issuing banks. Many code 05 declines clustered on one bank can indicate that issuer is flagging your MCC as high-risk. Beast's own decline-code work found that identifying such systemic patterns reduced client decline rates by 5 to 10%.

BIN-level opacity is exactly why this is hard. BIN configuration directly influences success at checkout. It can quietly tank approval by mis-flagging legitimate transactions. These gaps do not show up in top-line dashboards. A processor with a strong blended auth rate has little incentive to surface the BIN ranges where it underperforms. So you must request issuer-level and BIN-level reason codes from each payment service provider (PSP). Say a BIN has a 40% decline rate with one processor but 15% with another. That is actionable routing intelligence.

Modern orchestration tracks approval by provider, issuer, geography, amount band, and time of day. So analytics can tell you whether a drop is issuer behavior, routing, MID health, card type, 3-D Secure (3DS) friction, or configuration. That is the point of a per-issuer and per-BIN breakdown. It separates the issuer or MCC rule from everything else that can look like the same decline.

Levers that reduce MCC-driven declines

MCC declines are hard, so the levers are structural, not retry-first. Three move them: fix the MCC itself, restructure MIDs and routing, and triage retries by decline type. Blanket resubmission does the opposite of help here.

Start with the MCC. Confirm the code on the account matches your actual business. If it does not, request a change or open an account with the correct code. Correct MCC configuration removes a systematic authorization-rate ceiling. No amount of routing, tokenization, or retry logic can compensate for it. Solidgate reports MCC alignment across acquirers delivered a +5 to 7 percentage-point approval lift for a client with no product changes, no checkout redesign, and no engineering work.

Next, structure MIDs and routing. Operating multiple merchant accounts under different MCCs lets you recapture sales that come back as issuer declines under one MCC. You cascade the same transaction to a MID registered under a different code with a better issuer relationship. Cascading a declined front-end transaction to a backup processor with a different MCC can recover 3 to 5% of declines. Different acquiring banks have different relationships with issuers. Multi-MID routing typically splits volume by product category, geography, and chargeback concentration.

- Local acquiring on its own can add +10 to 20% approval rate.

- Cascade routing (instant retry via a different acquirer) recovers 3 to 8%.

- Scheduled retry of soft declines within 24 to 48 hours recovers 10 to 15%.

- Together these can lift card approval from roughly 70% to roughly 85%.

Then triage retries by type. Hard declines need a new payment method. Soft declines need better timing. Mastercard Merchant Advice Codes (MACs) tell you which. MAC 03 ("do not try again") and MAC 21 mean stop. MAC 24 through 30 specify wait windows from one hour to ten days. Retrying after a "do not retry" MAC is one of the fastest paths to excessive-retry violations. Layer in network tokenization, which can improve acceptance up to 15%. Also layer in intelligent retry, which yields a +11.6% average lifetime-value (LTV) lift with 51 to 67% better first-retry conversion.

When MCC declines signal a monitoring-program or compliance risk

A cluster of MCC declines can be a symptom of a deeper compliance problem. High-integrity-risk MCCs are exactly the categories that generate the most disputes and fraud. Those same disputes and fraud push your MID toward network monitoring thresholds. When declines and disputes rise on the same MCC, treat it as a portfolio-risk signal, not just a recovery problem.

Visa consolidated its dispute and fraud programs into the Visa Acquirer Monitoring Program (VAMP), effective April 1, 2025. So fraud and disputes now count together against one ratio: (fraud reports (TC40) + disputes (TC15)) / settled transactions (TC05). The merchant "excessive" threshold was 2.2% with a 1,500-event monthly floor. On April 1, 2026 it drops to 1.5% for the US, Canada, EU, and APAC. The ratio is count-based. So one MCC or issuer that drives elevated fraud can pull your whole portfolio toward the threshold.

Mastercard's Excessive Chargeback Merchant (ECM) program triggers at 100 to 299 monthly chargebacks and a 1.5 to 2.99% ratio. It escalates to High ECM (HECM) at 300+ and 3%+. These designations apply per MID. So isolating which MID (and its MCC) is breaching the ratio matters for both diagnosis and defense. Fines escalate from EUR/USD 1,000 up to 100,000 (ECM) or 200,000 (HECM) after 19+ months.

One lever keeps an MCC's ratio in check. TC40 fraud reports always count toward VAMP. TC15 disputes are excluded when you resolve them early through Verifi RDR, Verifi CDRN, or Ethoca Alerts. Deflecting disputes before they post keeps the same MCC that draws decline scrutiny from also breaching monitoring thresholds.

- Confirm the exact decline: is it a hard code (57, 62, 5C, 204) or a generic 05 that needs segmenting?

- Verify the MCC on each account matches your actual business, and request a change if it is mislabeled.

- Pull declines and group by decline code; rank the top five by volume.

- Break declines down by issuing bank and BIN to spot issuer-clustered or single-BIN patterns.

- Compare the same BIN across processors to find where routing recovers approvals.

- Set up a backup MID under a different MCC and cascade issuer declines to it.

- Triage retries by type: new payment method for hard declines, code-timed retry for soft ones; respect MAC and reattempt caps.

- Track fraud-plus-dispute ratio per MID against VAMP and ECM thresholds.

Frequently Asked Questions

What does "issuer declined mcc" actually mean?

It means the cardholder's bank refused the transaction specifically because of your merchant category code, not because of the card. Either the bank blocks that category as high-risk, or the merchant account was set up with the wrong MCC. It is a hard decline that persists until the card permission or the MCC changes.

Can I just retry an MCC decline?

No. MCC-related declines are always hard, so retrying the same card at the same MID will not recover them and only wastes attempts. Both Visa and Mastercard cap retries at 15 per card per 30-day window and fine excess reattempts, so blanket resubmission of a hard block is both futile and billable.

How do I tell an MCC decline from an insufficient-funds or Do Not Honor decline?

Read the code and the pattern. Code 51 is a soft, retryable funds decline; code 57 or Visa's 5C signals a permission or issuer-rule restriction. Code 05 is generic, so you isolate it by segmenting: many 05 declines clustered on one issuing bank often mean that bank is flagging your MCC.

Which MCCs get declined the most?

High-integrity-risk categories under Visa's VIRP draw the most scrutiny, including MCC 5967 (adult), 7995 (gambling), 7273 (dating), 5968 (subscription/direct marketing), and 5993 (tobacco). A transaction under MCC 5968 is 259% more likely to decline than the same one under a software-store MCC.

What fixes an MCC decline if retrying does not?

Structural levers. Confirm the MCC matches your business and correct it if not, since MCC alignment alone can add 5 to 7 points of approval. Then cascade declines to a backup MID under a different MCC with a better issuer relationship, and triage retries by decline type using Mastercard advice codes for timing.

Can MCC declines create a compliance problem?

Yes. The same high-scrutiny MCCs that draw declines also generate the most disputes and fraud, which push your MID toward Visa's VAMP and Mastercard's ECM thresholds. Because those ratios count fraud and disputes together per MID, one problem category can pull your whole portfolio toward monitoring and fines.