Network Tokenization vs. Account Updater: Which One Actually Keeps More Cards Active?

Network tokenization vs. account updater: both reduce failed payments by keeping card credentials current. Compare how credit card account updater and card network tokenization work, auth rate lifts, and which to implement first.

Why Do Stored Card Credentials Go Stale, and Why Does It Cost You Revenue?

Stored card credentials fail silently. That is the problem. A customer signed up 14 months ago, their bank replaced their card due to fraud, and the next time your billing system fires, the transaction hits a wall using credentials that no longer exist.

Approximately 33–40% of cards are reissued in any given year, according to Stripe's research on card‑reissue behavior. Reissues occur because of expiry, fraud‑related replacements, lost or stolen cards, and bank‑portfolio migrations. Every one of those stored PANs in your vault represents a future failed payment that has not yet been reconciled.

The pattern I see consistently: authorization rates look healthy in aggregate until someone runs a cohort analysis by card enrollment date. Cards older than 18 months fail at nearly double the rate of cards enrolled in the last six months. That gap is not a processor problem or a retry logic problem. It is a card data problem.

Two technologies exist specifically to close it: network tokenization and card account updater.

Understanding which one to use first, and how they interact, is the difference between recovering that revenue and watching it leak into involuntary churn quarter after quarter.

What Is Network Tokenization, and What Does It Actually Do?

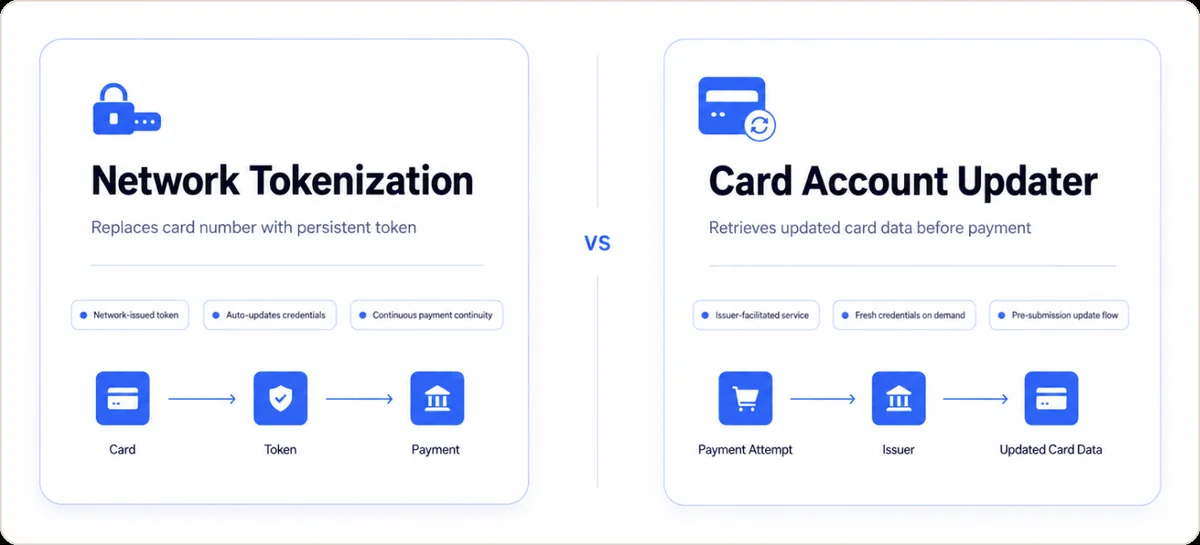

Network tokenization is a card-network-level process where Visa, Mastercard, or American Express replaces a card's primary account number (PAN) with a unique, network-issued token bound to a specific merchant or device. The token cannot be used anywhere else. It is meaningless outside the domain it was created for.

The key distinction from other forms of tokenization: the card network owns the token. When a card is reissued, the network automatically updates the token mapping without the merchant doing anything. The billing system fires the same token. The network resolves it to the new card. The payment goes through. No intervention required.

Beyond lifecycle management, network tokens carry a cryptogram, a one-time-use authentication value generated per transaction. This is why issuers treat token-based transactions as lower risk. The cryptogram signals that the payment originated from a trusted, provisioned source, not from scraped or compromised card data.

According to Visa's Adyen case‑study data, merchants using network tokens see an authorization‑rate uplift in the range of 2–7% over PAN‑based transactions, with an average improvement of about 3% on Adyen's platform. Pagos, which aggregates performance across its merchant base, similarly reports that enabling network tokens typically lifts authorization rates by roughly 2–7%, depending on issuer mix, card‑file age, and whether transactions are digital‑only. If your authorization rate is degrading and you have not run an approval rate drop analysis, start there before assuming network tokenization alone will solve the problem.

Network tokenization also directly reduces card-not-present fraud. Primer, citing Visa's internal network data, documents a fraud reduction of approximately 26% for network token transactions compared to raw PAN transactions. Lower fraud rates feed back into issuer approval logic, which means more approvals at the authorization stage, not just fewer chargebacks after the fact.

IXOPAY reports that network tokenization can improve authorization rates by +4%. According to industry data, 80 to 90% of major card-issuing banks across the US, EU, and Australia support network tokenization (Source).

What Is Card Account Updater, and When Is It the Right Tool?

Card account updater (AU) is an issuer-facilitated service that lets merchants query Visa or Mastercard for updated card credentials before submitting a transaction. Visa's version is called Visa Account Updater (VAU). Mastercard's is called the Automatic Billing Updater (ABU). The merchant or processor sends a card reference, the network queries the issuing bank, and returns an updated PAN or expiry date if the card has been reissued.

Account updater works with raw PANs. It does not replace the card number. It refreshes it. Two delivery models exist: batch mode runs queries overnight or weekly, refreshing your vault before the next billing cycle; real-time AU queries the network immediately before each transaction attempt. Real-time is measurably better for high-value subscription accounts, where a single failed renewal triggers a failed payment recovery workflow that costs more in overhead than the query fee.

Stripe's case study on Zapier reported that Card Account Updater contributed 2.76% of the authorization-rate uplift. Checkout.com's real-time account updater is a separate product; any comparison should distinguish real-time updates from batch updater delivery.

For merchants with large legacy card vaults built before token capability existed, the account updater is not a fallback. It is the primary tool. Every raw PAN in your vault that pre-dates your token enrollment is a card account updater that a card account updater can update and network tokenization cannot touch until a token is provisioned for it.

Account updater has a hard limit: it only returns what the issuer reports. Closed accounts with no replacement, cards from issuers not enrolled in VAU or ABU, and cards from markets where the program is not active return nothing.

Network Tokenization vs. Card Account Updater: A Direct Comparison

| Feature | Network Tokenization | Card Account Updater |

|---|---|---|

| What gets updated | Token mapping, auto-refreshed by card network | PAN and expiry, retrieved from issuing bank |

| Update mechanism | Real-time, automatic on card reissue | Batch (nightly/weekly) or real-time API per transaction |

| Works with legacy PAN vault | No. Requires token provisioning per card | Yes. Works directly with stored raw PANs |

| Fraud reduction | Approximately 26% reduction in CNP fraud (Visa data) | None. PAN-based, no authentication layer |

| Authorization rate lift | 2 to 7% depending on issuer mix and vertical | 1 to 3.3% depending on delivery mode |

| PCI DSS scope impact | Reduces scope. Token replaces PAN in merchant vault | No change to PCI scope |

| Interchange incentives | Yes. Visa and Mastercard offer 5 to 10 bps savings | No interchange benefit |

| Issuer coverage | 80 to 90% of major US, EU, and AU issuers | Broader for legacy cards. Dependent on VAU/ABU enrollment |

| Best starting point | New card enrollments, digital-first billing flows | Legacy vaults, cards stored before token adoption |

| Requires network enrollment | Yes, per card scheme (Visa Token Service, MDES) | Yes, separate program enrollment per network |

The structural difference: network tokenization changes what gets stored and how it authenticates. Account updater refreshes what is already stored. One is architectural. The other is operational. Both are necessary because they address different parts of the same problem.

If You Can Only Start with One, Which Should You Choose?

This is the question most posts refuse to answer directly.

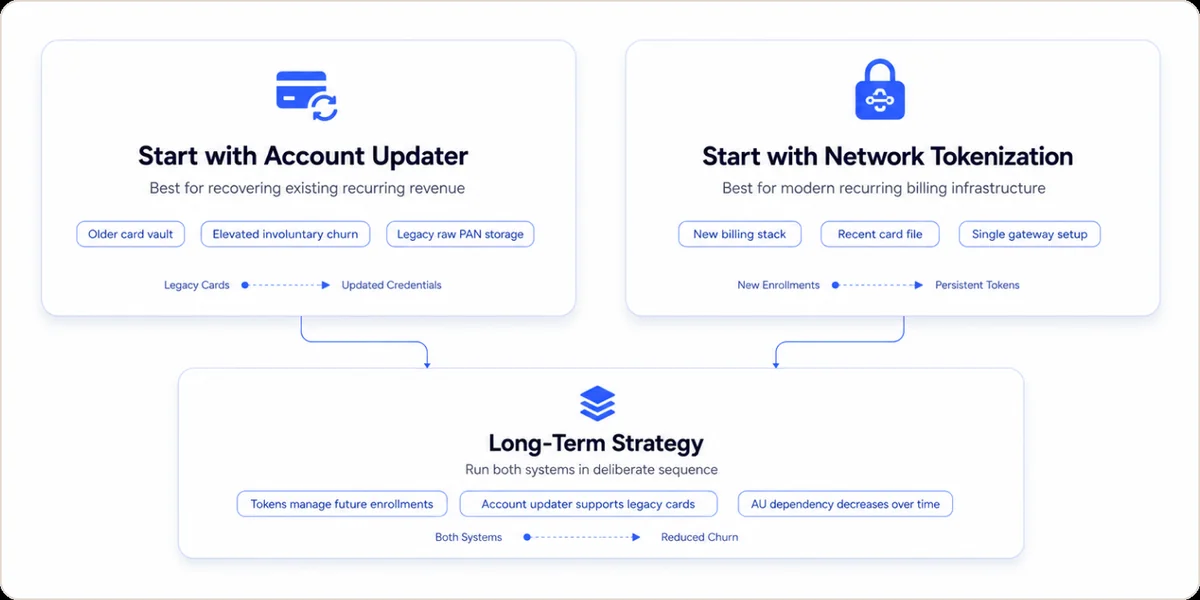

Start with account updater if: Your card file is more than 12 months old, your vault holds raw PANs from before token capability existed, or your involuntary churn rate is already elevated and you need the fastest path to recovering existing revenue. Account updater refreshes credentials across your existing base without requiring re-enrollment at checkout.

Start with network tokenization if: You are building or rebuilding your recurring billing infrastructure, your card file is relatively recent, or you process primarily through a single gateway that already manages token provisioning.

The honest answer for most merchants at scale: run both in deliberate sequence. Tokens handle forward-going enrollments. Account updater handles the legacy tail. As your token-enrolled base grows, the AU dependency shrinks. But it never reaches zero, and the account updater is never fully redundant.

Peter Karpas, CEO of Boost Payment Solutions, said that while the payments industry has built a strong digital infrastructure, the biggest challenge remains the "last mile" — keeping payment credentials current when the customer is not physically present. (Source)

Is Network Tokenization Required by PCI DSS?

Network tokenization is not required by PCI DSS, but it directly reduces your PCI scope. When a card network token replaces a raw PAN in your vault, the merchant environment no longer stores, transmits, or processes actual card numbers. That removes systems from the PCI DSS scope.

Account updater has no effect on PCI scope. Because it operates on raw PANs, any system that calls AU or stores the resulting updated PAN remains fully within PCI scope.

For merchants navigating a PCI DSS compliance audit or planning a PCI DSS compliance checklist review, the token-first approach reduces the compliance surface and the operational cost of maintaining it. That is a secondary benefit of network tokenization that most ROI calculations undercount.

What Does the Retry Logic Look Like When Both Tools Are Running?

This is what the payment flow looks like when both tools are deployed correctly:

- The transaction is submitted using the network token for a stored card.

- If the token is approved, the payment succeeds.

- If the token is declined, the system falls back to the stored raw PAN.

- Before retrying on PAN, the system queries account updater to confirm the PAN is current.

- If AU returns an updated PAN, the retry uses the refreshed credentials.

- If AU returns nothing, the system routes to a dunning management or failed payment recovery flow.

This is the layered architecture that Juspay, Spreedly, and Pagos all describe as best practice. Running one tool without the other removes a layer. Silent declines with no retry loop leave recoverable revenue on the table in every billing cycle.

For merchants running multiple processors, a payment orchestration layer centralizes token and AU status across acquirers, rather than configuring fallback logic separately per gateway.

What Do the Real-World Numbers Say?

Stripe's network tokens and card account updater tools help ensure we don't encounter that problem, and enabled us to increase subscription auth rates by over 4%. That is both tools in sequence, not either in isolation.

Juspay reported that Checkout.com saw a 3.3% acceptance-rate uplift after enabling Real-Time Account Updater on tokenized cards. Visa's published VisaNet data shows a 3% card authorization rate lift from network tokenization (global average, card-not-present transactions).

At a $50 million annual subscription revenue baseline running at a 91% authorization rate, closing a combined 4% gap recovers approximately $2.2 million in annual revenue currently leaking through stale card credentials (Source).

A 2022 Mastercard industry report on recurring billing documented that payment credential failures account for approximately 40% of involuntary subscription churn. Network tokenization and account updater together are the only technical stack that directly addresses that 40%. Retry logic, dunning management, and customer notifications address the symptom. These two tools address the cause.

How to Get Both Tools Running Without Overcomplicating It

Most merchants do not need to integrate directly with Visa Token Service or Mastercard MDES. Stripe, Adyen, Braintree, Checkout.com, and Spreedly all manage token provisioning as part of their vault. Enabling network tokenization is often a configuration change, not a development project, if you are already using one of those processors. Account updater is similarly a feature toggle in most major gateways, though it carries a per-card query fee that varies by processor and volume.

For merchants running across multiple acquirers, a multi-acquirer strategy that centralizes token and AU management prevents inconsistent retry behavior across processors. Inconsistency in the retry layer is where recoverable revenue disappears without any visibility in your reporting.

Three things to handle before going live. First, audit your existing card vault. Cards stored as raw PANs before your token capability went live need an account updater pass before your next billing cycle, not after. This is the most commonly skipped step. Second, set the retry order explicitly: token attempt first, AU-checked PAN retry second, recovery flow third. Third, track authorization rates by card enrollment cohort, not just in aggregate. Aggregate rates mask the card vintage problem entirely.

The Bottom Line: What Should You Actually Do Next?

Network tokenization is a structural investment. It changes how credentials are stored, authenticated, and maintained automatically over time. Card account updater is the operational safety net. It keeps your existing vault accurate for cards that fall outside the token network and for legacy data that was never provisioned as a token.

The decision is not which one to prioritize indefinitely. The decision is which one you are missing right now and how quickly you can layer the other on top.

If your authorization rate is declining on older card cohorts, account updater is the fastest lever. If you are building or rebuilding your recurring billing stack, start with network tokenization. If you are processing more than $5M annually in subscription revenue and running neither, you are losing recoverable revenue in every billing cycle.

Start by reviewing your authorization rate by card enrollment cohort. If you do not have that visibility, that is the first gap. The data will tell you which tool to prioritize and where your vault is most exposed.

Frequently Asked Questions

What is network tokenization?

Network tokenization is a process where Visa, Mastercard, or American Express replaces a card's actual account number with a unique, network-managed token. The token automatically updates when the underlying card is reissued, without merchant intervention.

What is card account updater?

Card account updater is an issuer-facilitated service that retrieves updated card numbers or expiry dates from issuing banks before a payment is submitted. Visa's version is called VAU (Visa Account Updater) and Mastercard's is called ABU (Automatic Billing Updater).

Is network tokenization the same as account updater?

No. Network tokenization replaces the card number with a token that auto-updates. Account updater fetches a refreshed PAN and expiry from the issuing bank on request. Tokenization is structural. Account updater is operational. They solve the same root problem through different mechanisms.

Do I need both network tokenization and account updater?

Yes, for subscription businesses. Network tokenization covers approximately 80 to 90% of major issuers automatically. Account updater covers legacy card files and issuers not yet in the token network. Running both together produces meaningfully better authorization rates than either tool alone.

Which should I implement first: network tokenization or account updater?

If your card vault is more than 12 months old and holds raw PANs, start with account updater to recover existing credentials. If you are building a new recurring billing flow, start with network tokenization. Most merchants at scale need both running in sequence within the same payment flow.

Does account updater reduce fraud?

No. Account updater refreshes card data and has no fraud prevention function. Network tokenization reduces card-not-present fraud by approximately 26%, according to Visa's published data, because each token transaction includes a cryptogram that authenticates the payment source.

Is network tokenization required by PCI DSS?

Network tokenization is not required by PCI DSS, but it reduces PCI scope by replacing raw PANs in the merchant vault with tokens. Account updater does not affect PCI scope because it operates on raw card data throughout.

What happens when a network token fails?

A failed token should trigger a fallback to the stored PAN. Before retrying, run an account updater query to confirm the PAN is current. If AU returns nothing, route to a failed payment recovery or dunning flow. Silent declines without this retry sequence lose recoverable revenue in every billing cycle.