Multiple Payment Gateways: The Routing Strategy That Recovers Up to 15% in Lost Authorization Revenue

Learn how a multiple payment gateway strategy recovers lost authorization revenue, reduces processing fees by 8%, and eliminates single-point-of-failure risk.

What Is a Multiple Payment Gateway, and Why Does It Matter?

A multiple payment gateway strategy connects a merchant to two or more payment processors simultaneously, using routing logic to send each transaction to the gateway most likely to approve it at the lowest cost. When one gateway fails or returns a soft decline, traffic shifts automatically to a backup processor before the customer sees any interruption.

The economics are concrete. Visa and Mastercard data suggest that approximately 15% of recurring transactions are declined. Cited by Chargebacks911, a meaningful portion of those declines is soft failures: processor timeouts, issuer-side fraud filter over-triggers, and network routing errors that have nothing to do with a customer's available funds.

Spreedly's published case study data details two merchants benefiting from adding processors: Company A improved from 86% to 93% authorization rate (not 88%), recovering an extra $2 million in weekly revenue from 121K average transactions. Company C, with high volume and lower spend per transaction, boosted success by 8% (from around 88% implied) using more gateways, gaining $354K per week that could have been lost.

Merchants who treat gateway infrastructure as a back-office utility lose recoverable revenue every single day. The ones who treat routing as a performance layer compound that advantage with every percentage point of improvement. Understanding how credit card decline codes map to soft versus hard failures is the first step to knowing exactly what your current setup is leaving on the table.

What Are the Core Benefits of Multiple Payment Options for Merchants?

The benefits of multiple payment options fall into three categories: revenue protection, cost reduction, and international market access. Each addresses a distinct failure mode of single-processor dependency.

Does Integrating Multiple Payment Gateways Actually Protect Revenue?

Yes. When failover logic routes a soft-declined transaction to a secondary processor within milliseconds, the customer sees an approval, not a rejection. Spreedly's analysis of over 100 million transactions across 114 processors and 106 currencies confirmed that gateway performance varies significantly by card type, currency, and geography. A processor that approves 94% of domestic transactions may only approve 78% of international transactions from the same card brand. Routing logic captures both peaks simultaneously.

For a diagnostic breakdown of how the authorization rate drops signals systemic routing problems, the approval rate drop analysis covers the method used across high-volume merchant accounts.

How Much Do Multiple Gateways Actually Reduce Processing Fees?

Competitive routing cuts blended processing fees by up to 8% by directing each transaction to the processor with the lowest effective cost for that specific card type. For a merchant processing $10 million annually, that is $800,000 returned to operating margin through architecture, not renegotiation.

Blended pricing, typically 2.9% plus $0.30 per transaction, obscures the real cost of processing different card categories. A domestic debit transaction costs significantly less at interchange than a premium rewards credit card, but blended pricing charges the same flat rate for both.

Routing domestic debit to the processor with the lowest debit markup and international credit to the provider with better cross-border settlement rates captures that differential systematically. The profitability analysis framework applies this model to specific revenue mixes for merchants building an internal business case.

Does Offering Multiple Payment Options Improve International Conversion?

The Baymard Institute's checkout research establishes that roughly 70% of online shopping carts are abandoned on average, and international complexity accelerates that rate considerably. When merchants do not offer local payment methods at checkout, cross-border conversion collapses.

Adding regional processors that support SEPA in Europe, UPI in India, or Alipay in China directly addresses the most common reason international shoppers abandon: unfamiliar or unavailable payment options.

A multi-processor setup enables entry into new geographies up to three times faster because compliance, foreign exchange handling, and local settlement rails are pre-abstracted through the orchestration layer, rather than requiring country-by-country direct integration.

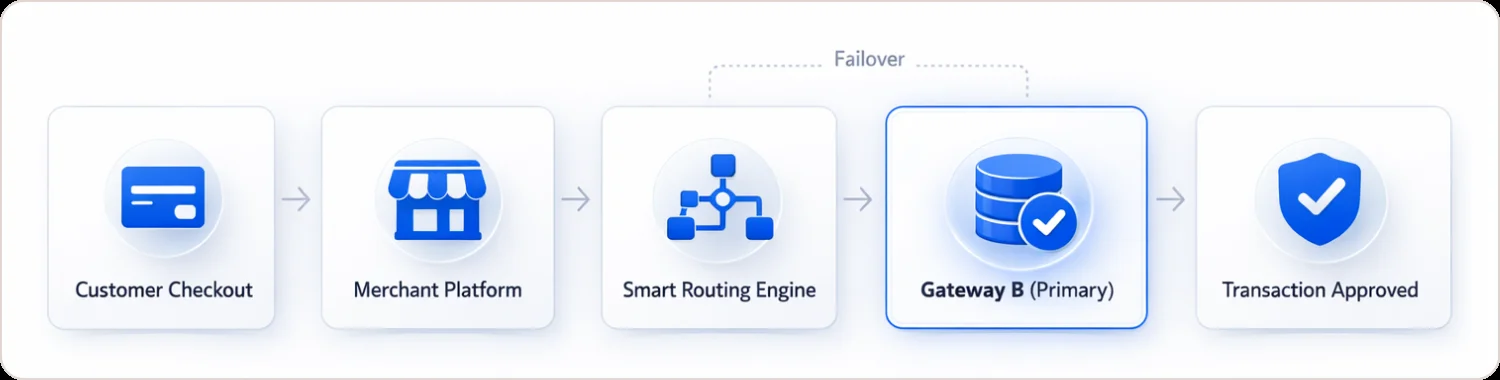

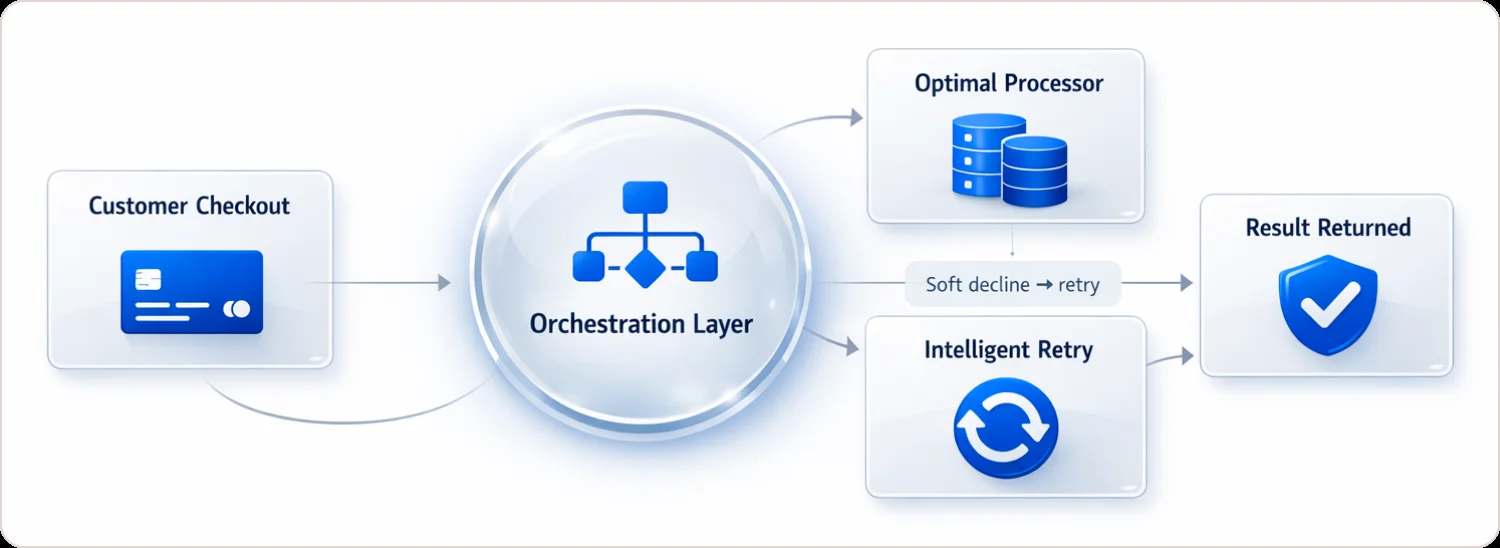

How Does Multiple Payment Gateway Integration Work in Practice?

Multiple payment gateway integration connects a checkout environment to several processors through a payment orchestration platform (POP). The POP manages routing rules, failover logic, and token storage through a single unified API rather than requiring separate hardcoded connections to each processor.

Here is exactly how a transaction flows through an orchestrated setup:

- A customer submits card details at checkout.

- The orchestration layer evaluates routing rules: card type, BIN range, geography, transaction size, and historical success rates for that card profile at each connected processor.

- The transaction is sent to the optimal processor.

- If that processor returns a soft decline, the system retries on the next gateway in the hierarchy within milliseconds, with no visible interruption to the customer session.

- The approved or final declined result is returned to the checkout.

The infrastructure element that makes this genuinely portable is the agnostic token vault. Card data is tokenized and stored independently of any single processor. Replace one gateway with another, and store customer payment methods transfer without requiring customers to re-enter card details. Without an agnostic vault, switching processors forces a full re-onboarding event that creates its own churn.

Multiple Payment Gateway vs. Single Gateway: Which Is Right for Your Business?

| Factor | Single Gateway | Multiple Payment Gateways |

|---|---|---|

| Authorization Rate | ~85% average | Up to 93% to 97% with smart routing |

| Downtime Risk | High, single point of failure | Low, automatic failover to backup |

| Processing Cost | Fixed blended rate | Up to 8% lower via competitive routing |

| Global Payment Coverage | Limited to primary processor | Broad, via regional processors |

| Setup Complexity | Low | Medium, centralized via orchestration POP |

| PCI DSS Scope | Per-gateway | Centralized via agnostic vault |

| Vendor Lock-in | High | Eliminated |

| Reconciliation | Manual, manageable at low volume | Requires automation tooling at scale |

| VDCAP Readiness (April 2026) | Requires per-gateway rebuild | Captured automatically via orchestration layer |

A single gateway is only reasonable when transaction volume is low, customers are purely domestic, and processing fees are not a material cost line. For any merchant processing more than $1 million annually, selling across more than one country, or running subscription billing, an orchestrated multi-processor setup generates measurable ROI within the first quarter.

What Is Smart Routing, and How Does It Maximize Authorization Rates?

Smart routing is the decision engine inside a payment orchestration platform that selects the optimal processor for each transaction in real time, based on card-level performance data, historical success rates, and cost parameters. Smart routing maximizes authorization rates by matching each transaction's profile to the processor statistically most likely to approve it.

The routing variables that produce meaningful lift include card type, network, and issuing bank BIN range; transaction currency and customer geography; issuer-specific decline patterns by time of day and card brand; and transaction size relative to each processor's fraud threshold configuration.

Spreedly's analysis of 155 processors across 147 currencies, published on their data platform, confirms that the top-performing processor for one currency is consistently not the top performer for another. The data.spreedly.com platform publishes authorization performance data monthly, making processor selection a data-driven decision rather than a contractual one.

The formula for expected revenue recovery from an authorization lift is:

Our payment routing optimization service applies this model to live transaction data to identify the actual lift available in a specific configuration.

What Does Integrating Multiple Payment Gateways Actually Cost?

| Pricing Model | Typical Rate | Best For | Transparency | Net Cost at Volume |

|---|---|---|---|---|

| Blended | 2.9% + $0.30/transaction | Merchants under $500K/yr | Low, card-type costs hidden | Higher; debit subsidizes premium rewards |

| Interchange-Plus | Interchange + 0.10–0.25% + $0.10 | Growth-stage and enterprise | High, line-item cost visibility | 15% to 30% lower than blended at scale |

| Flat Rate per Processor | $0.05 to $0.15/transaction | Predictable mid-volume | Medium | Variable by card mix |

| Orchestration Platform | Gateway fees + $0.02–0.10/transaction | Multi-gateway operators | High, centralized | Lowest overall; routing savings exceed POP fee |

Interchange-plus pricing passes the actual network interchange rate to the merchant with a fixed markup. At high volumes, it consistently outperforms blended pricing because the markup on low-cost debit no longer subsidizes premium travel rewards cards. A payment orchestration platform adds $0.02 to $0.10 per transaction on top of gateway fees. At meaningful volume, the authorization lift and routing savings recover that cost within the first month.

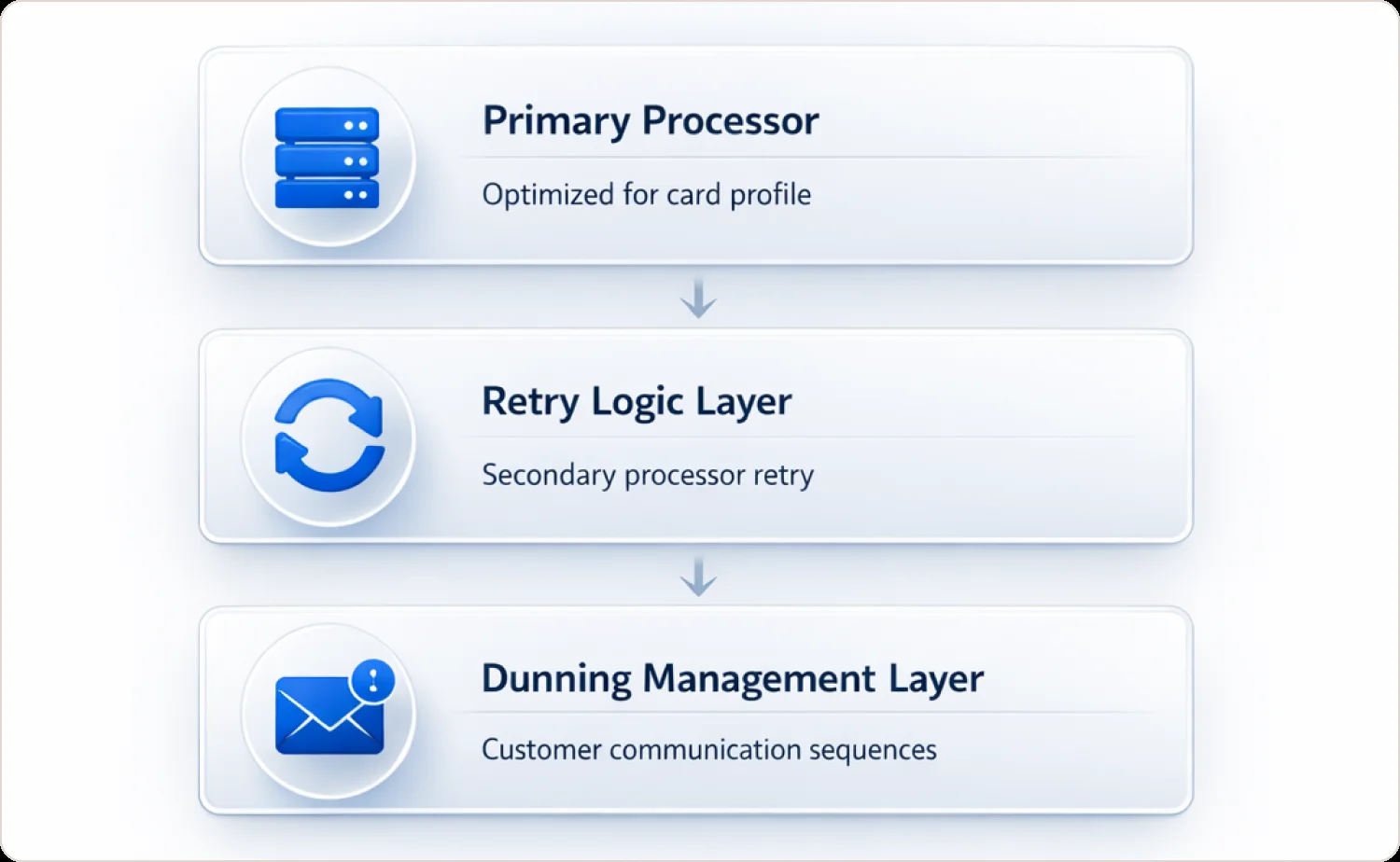

How Should Subscription Businesses Integrate Multiple Payment Gateways to Stop Involuntary Churn?

Subscription businesses should implement a gateway hierarchy that routes each recurring charge to the processor with the highest historical approval rate for that specific card, billing cycle, and currency. This approach reduces involuntary churn caused by payment failures rather than genuine cancellations.

Recurly's research across thousands of subscription businesses shows that 20-40% of churn is involuntary, meaning customers never intended to cancel. Their industry analysis estimates inadequate churn management costs the global subscription industry $129 billion annually in failed payment losses. Recurly's platform delivers an average 8.6% revenue lift for businesses using intelligent churn management, including dynamic gateway routing.

Implementation follows three layers: a primary processor optimized for that card profile handles the initial charge; a retry logic layer re-attempts on a secondary processor before surfacing a failure to the customer; and a dunning management layer handles persistent failures with communication sequences.

Our payment retry strategies guide covers sequencing and timing rules that produce the highest recovery rates without triggering issuer-side fraud flags. The involuntary churn recovery framework maps that approach to specific subscription models.

What Does the April 2026 Visa VDCAP Program Mean for Merchants Running Multiple Gateways?

The Visa Digital Commerce Authentication Program (VDCAP), launching in April 2026, offers merchants a direct interchange fee reduction of 0.05% for submitting high-quality authentication data such as Device ID, IP address, email, and billing address. This reduction increases to 0.10% when combined with Network Tokens in the US. The program incentivizes better data quality to improve authorization rates and reduce fraud in digital commerce. (Source)

Merchants using a payment orchestration platform are best positioned to capture these savings. The orchestration layer captures the full required data payload once and passes it across every connected processor simultaneously. Merchants on direct, hardcoded integrations face per-processor implementation work that most will not complete before the April 2026 deadline.

The risk extends beyond missed savings. As ISO 20022 data field requirements tighten through late 2026, absent authentication data will trigger hard declines on transactions that currently soft-decline and recover through retry logic. That is permanent revenue loss, not a deferred compliance task.

Our gateway compliance monitoring service tracks readiness against VDCAP and ISO 20022 requirements in real time, and the 3D Secure authentication guide covers the integration steps required before the April deadline.

How Do You Reconcile Transactions Across Multiple Payment Gateways?

Reconciliation across multiple payment gateways requires automated software that aggregates transaction records from all processors into a single ledger, matches each payment against its corresponding invoice or order, and flags discrepancies in real time. Manual reconciliation across three or more gateway dashboards typically consumes three to four full working days per month.

Each processor records fees, refunds, and settlements in different formats, at different timestamps, and against different reference identifiers. At scale, these differences generate revenue leakage that compounds monthly.

The automated workflow that eliminates this follows four core steps: aggregate all transaction data on a defined schedule, run automated matching against internal orders by amount and reference ID, flag discrepancies in real time for structured investigation, and generate a monthly summary for financial close with a full audit trail.

Automated reconciliation tools reduce operational costs in this function by up to 90% versus manual processes. For a business with $20 million in annual payment volume, a 3% reduction in reconciliation leakage recovers $600,000 annually from errors that manual review routinely misses.

Conclusion: Three Problems, One Infrastructure Decision

Single-gateway dependency creates three separate revenue problems simultaneously: it loses soft-declined transactions that a second processor would approve, it overpays on processing fees by hiding card-type cost variance inside blended pricing, and it locks card data inside one vendor's tokenization environment with no portable exit.

When merchants integrate multiple payment gateways through an orchestration platform, all three problems are resolved through one API connection, one token vault, and one routing configuration layer. The Spreedly data is clear: multiple payment gateway integration lifts authorization rates by 5 to 8 percentage points. Recurly's research is clear: 20% to 40% of subscription churn is involuntary and recoverable. The April 2026 Visa VDCAP program creates a hard deadline: merchants without authenticated data submission across all connected processors will face permanent hard declines on transactions that currently recover.

The sequencing that produces the fastest ROI: implement a payment orchestration platform with an agnostic token vault, connect the primary processor, add a secondary optimized for the card type generating the highest current decline rate, configure failover logic before layering smart routing rules, and automate reconciliation from day one. Subscription businesses should add intelligent retry logic before any other optimization.

A multiple payment gateway strategy is not a complexity trade-off. It is the infrastructure decision that determines how much recoverable revenue actually clears to the balance sheet.

Frequently Asked Questions

What is a multiple payment gateway?

A multiple payment gateway connects a merchant to two or more processors simultaneously, using routing logic to approve each transaction and automatic failover when the primary processor declines.

How does integrating multiple payment gateways improve conversion rates?

Failover logic re-routes soft-declined transactions to a secondary processor before the customer sees a rejection, lifting authorization rates by 5 to 8 percentage points (Spreedly).

What are the benefits of multiple payment options for e-commerce merchants?

Higher authorization rates, lower processing fees through competitive routing, access to local payment methods that reduce international abandonment, and no single point of failure.

Multiple payment gateway vs. payment orchestration platform: what is the difference?

Multiple payment gateways are the outcome; a payment orchestration platform (POP) is the technology layer that manages routing, token vault, monitoring, and reconciliation under one API.

How much does it cost to integrate multiple payment gateways?

An orchestration platform adds $0.02 to $0.10 per transaction; at volume, authorization lift and routing savings recover that fee within the first month.

When should a business implement multiple payment gateways?

When processing more than $1 million annually, selling internationally, or running subscription billing, a single gateway failure creates measurable churn.

How do multiple payment gateways help with chargebacks and disputes?

Orchestration routes high-risk profiles to the processor with the strongest fraud filtering and centralizes transaction data across all processors, strengthening evidence and supporting Visa VAMP compliance. Our chargeback management service integrates directly with multi-gateway data to intercept disputes before they escalate.